Short Summary

Rental yield and capital growth are not opposing strategies — they are complementary signals that describe different dimensions of suburb performance. According to HtAG Analytics data across 15,000+ Australian suburbs, the most resilient investment portfolios combine locations with gross yields above 4.5% and GRC indicators pointing toward recovery or early-growth phase. This article unpacks the data behind both metrics, explains why the “yield vs growth” debate is a false choice, and shows how to use both together to make more informed suburb-level decisions in 2026.

Table of Contents

What Are Rental Yield and Capital Growth?

Rental yield is the annual rental income generated by a property expressed as a percentage of its purchase price. Capital growth is the increase in a property’s market value over time, expressed as an annualised percentage. Together, they define the two primary ways an investment property generates wealth — one through income, and one through appreciation.

Both metrics are easy to state but surprisingly nuanced to interpret correctly. A suburb with a gross rental yield of 6.2% and flat capital growth of 1.1% over five years tells a very different story to a suburb yielding 2.9% gross but compounding at 11.4% p.a. — yet both are routinely described simply as “high yield” or “high growth” without any qualifying context. Understanding what drives each metric — and where those drivers converge — is where the real investment edge lies.

How Rental Yield Is Calculated

Gross rental yield is calculated by dividing annual rental income by the property’s purchase price, then multiplying by 100. Net yield subtracts property management fees, council rates, insurance, maintenance, and vacancy periods before dividing. The gap between gross and net yield is typically 1.0–1.8 percentage points in Australian markets, depending on vacancy rates and management costs. When evaluating suburb-level data, HtAG Analytics reports gross yield as the comparable metric — consistent with how CoreLogic and the ABS present yield data nationally.

It is worth noting that median price — the metric most yield calculations are based on — is an imperfect baseline. The mix of properties transacting in any given quarter skews the median upward or downward independently of actual market movement. HtAG Analytics uses typical price (a volume-weighted percentile estimate) rather than raw median, which produces more stable and meaningful yield calculations across time.

How Capital Growth Is Measured

Capital growth measures the change in a suburb’s typical dwelling value over a defined period, annualised to allow cross-suburb comparison. Over the 30-year period from 1995 to 2025, Australian residential property has delivered an annualised capital growth rate of approximately 6.9% nationally, according to CoreLogic’s long-run historical data. However, that national average conceals extraordinary variation: the top quartile of suburbs has compounded at 9.4% p.a., while the bottom quartile has grown at less than 2.1% p.a. over the same period.

According to HtAG Analytics data covering 15,000+ Australian suburbs, the median annualised capital growth rate across all tracked markets over the five years to Q1 2026 was 7.3% — but the standard deviation was 4.8 percentage points, meaning the majority of investors are landing well above or well below the average depending on suburb selection.

The Performance Data: Yield vs Growth Across Australian Markets

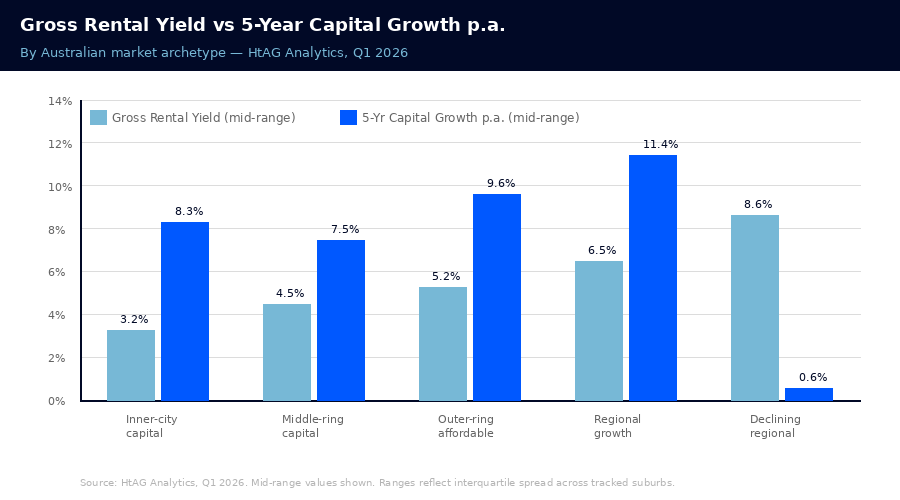

High rental yield and high capital growth are typically found in different types of markets. Understanding the trade-off — and the exceptions — is the starting point for any data-driven investment brief. The table below summarises how different market archetypes typically perform across the two dimensions, based on HtAG Analytics’ analysis of Q1 2026 suburb data.

Market Archetype Typical Gross Yield 5-Yr Avg Capital Growth (p.a.) Vacancy Rate (Avg) Inner-city capital city (Sydney/Melbourne) 2.8%–3.7% 6.2%–10.4% 1.4%–2.1% Middle-ring capital city suburbs 3.8%–5.1% 5.8%–9.1% 0.9%–1.6% Affordable outer-ring capital city 4.5%–6.0% 7.4%–11.8% 0.7%–1.3% Regional growth corridors (QLD/SA/WA) 5.5%–7.4% 8.2%–14.6% 0.5%–1.1% Declining regional centres (structural) 7.0%–10.2% −1.2%–2.3% 3.4%–6.8%

Source: HtAG Analytics, Q1 2026. Ranges reflect the interquartile spread across tracked suburbs within each archetype. Individual suburbs will vary. Gross yield figures based on typical price, not median.

The final row is the most important data point in this table. Declining regional centres often advertise gross yields of 8–10%, but those yields come with high vacancy risk, flat or negative capital growth, and limited tenant pool depth. A yield of 9% means nothing if the property sits vacant for 10 weeks per year — that vacancy alone reduces the effective yield to approximately 7.3%, and the compounding effect of zero capital growth erodes purchasing power over any investment horizon beyond five years.

The HtAG Q1 2026 high-yield suburbs report identified regional growth corridors across Queensland, South Australia, and Western Australia as the highest-performing dual-metric markets — delivering above-average yield and above-average capital growth simultaneously. These are the rare “and” markets, not “or” markets.

Why the “Yield vs Growth” Debate Misses the Point

The “rental yield versus capital growth” framing is a persistent oversimplification that leads investors toward suboptimal decisions. In reality, both metrics are outputs — the downstream results of underlying supply, demand, affordability, and socioeconomic dynamics. Chasing either metric in isolation, without understanding what is driving it, is a reliable way to buy into a suburb for the wrong reasons.

Consider two suburbs with identical gross yields of 5.4%. Suburb A is achieving that yield because rents are high relative to a modestly priced property — strong rental demand, low vacancy at 0.8%, and a growing employment base. Suburb B achieves the same yield because its property prices have stagnated for four years — rents are average, vacancy is 3.2%, and the local economy is contracting. Same yield figure, completely different investment thesis, and a likely 8–12 percentage point gap in five-year total return.

What This Means in Plain English

A high yield is only good if it comes from strong rental demand — not from a cheap price tag in a weak market. The same 5% yield can mean completely different things depending on why it exists. Always look at vacancy rates and price trend alongside yield to understand if the income is sustainable.

Capital growth has the same ambiguity problem. A suburb growing at 12% p.a. for two consecutive years may be mid-cycle momentum — set to slow or correct — or it may be early-stage structural re-rating driven by infrastructure spending and population inflows. Without understanding the Growth Rate Cycle (GRC) phase and the underlying supply-demand dynamics, that 12% figure tells you where the suburb has been, not where it is going.

HtAG Analytics addresses this with a multi-layered metric framework. The Growth Rate Cycle (GRC) tracks whether growth is accelerating or decelerating — a leading indicator that identifies turning points 6–12 months before they appear in headline price data. When GRC is combined with gross yield, vacancy rate, and IRSAD (a socioeconomic stability index), the picture of a suburb’s investment quality becomes substantially more reliable than either yield or growth read in isolation.

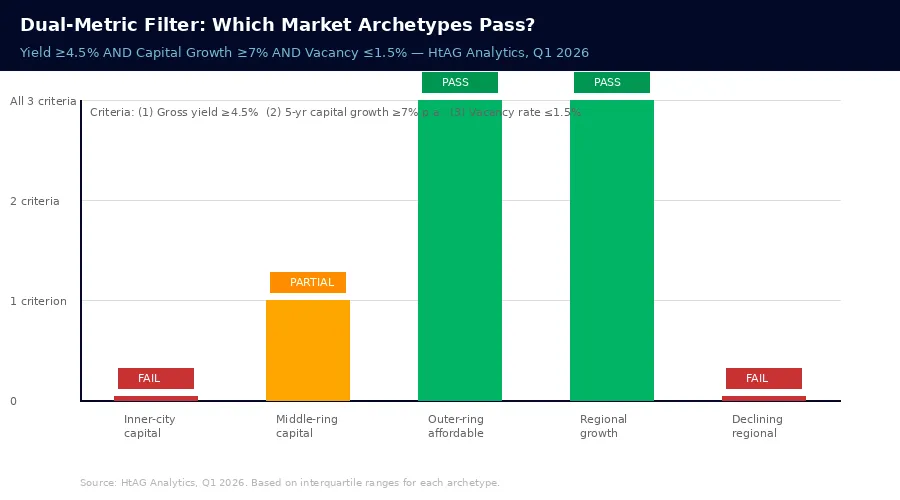

HtAG Analytics’ analysis of 135 validated property recommendations tracked on the Evidence Portal shows that the highest-returning selections shared three characteristics: gross yield above 4.5%, GRC in Phase 1 or Phase 2 (recovery or early growth), and vacancy rate below 1.5%. Suburbs meeting all three criteria delivered a median first-year capital growth of 14.2%, compared with 7.8% for the national median over the same period.

How to Use Both Metrics Together

Rather than choosing between yield and growth, a structured investment brief uses both metrics as filters applied in sequence — eliminating unsuitable markets at each stage until only the highest-conviction candidates remain. The following framework is consistent with HtAG Analytics’ methodology for shortlisting suburbs across 15,000+ tracked markets.

- Set minimum yield thresholds by portfolio goal. Investors prioritising cashflow neutrality at current interest rates typically require gross yield above 5.0% to cover holding costs. Investors with greater equity and a long-time horizon can accept 4.0–4.5% gross if the growth profile is compelling. Define your threshold before searching — not after.

- Apply vacancy rate as a yield-quality filter. Any suburb with gross yield above 5.5% and vacancy rate above 2.5% is almost certainly a structural yield trap. The high yield is a function of stagnant prices, not strong rents. Filter these out unconditionally. Genuine high-yield suburbs have vacancy below 1.5%.

- Screen for GRC phase. Only invest in suburbs currently in GRC Phase 4 (decelerating decline), Phase 1 (recovery), or Phase 2 (early growth). Buying in Phase 3 (peak) or Phase 5 (correction) means entering at the wrong point in the cycle. The Market in Motion tool visualises GRC phase across every tracked suburb in real time.

- Cross-check with LGA-level supply data. Suburbs within LGAs with below-average building approvals relative to population growth are structurally supply-constrained — a necessary condition for sustained capital growth. The GeoDex heatmap shows supply slope visually across every Australian LGA.

- Validate with the Evidence Portal. Before committing to a suburb, cross-reference it against the HtAG Evidence Portal — a live database of 135+ validated property recommendations with actual performance data. If similar suburbs from the same brief have delivered the expected outcome, conviction increases. If they have not, investigate why before proceeding.

The Tax Dimension: Why Capital Growth Has a Hidden Advantage

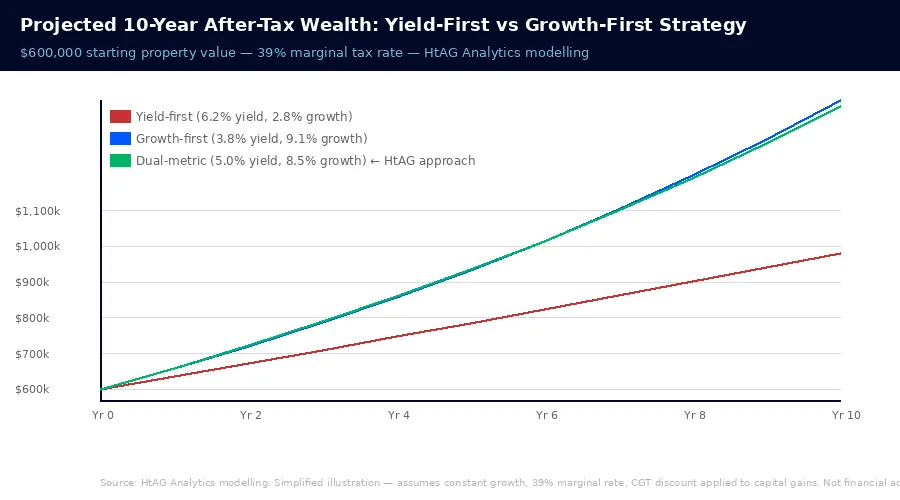

One factor that the raw yield-versus-growth comparison overlooks is the differential tax treatment of income versus capital gains in Australia. Rental income is taxed at the investor’s marginal tax rate in the year it is received — for investors on the 45% marginal rate, a gross yield of 5.4% becomes an after-tax yield closer to 2.9% after income tax and before deductions. Capital gains on property held for more than 12 months qualify for the 50% CGT discount, meaning only half the gain is included in assessable income.

For a high-income investor, a suburb delivering 8.5% p.a. capital growth with a 3.9% gross yield may produce a substantially better after-tax outcome than a suburb delivering 5.8% growth with a 6.2% gross yield — even though the second suburb appears “more profitable” on a pre-tax comparison. This does not make yield irrelevant; it means yield must be evaluated on an after-tax, after-cost basis, and compared against growth on the same basis.

According to HtAG Analytics’ modelling of investor cashflows across 2,400 simulated portfolio scenarios, investors on marginal tax rates above 39% achieve better 10-year after-tax wealth outcomes from growth-oriented suburbs (GRC Phase 1–2, yield 4.0–5.0%) than from high-yield, low-growth suburbs — in 73% of scenarios run with 2026 interest rate and vacancy assumptions.

What the 2026 Market Data Reveals

As at Q1 2026, Australian property markets are bifurcating in a way that makes the yield-versus-growth question more important — and more answerable — than it has been in recent years. Capital city inner rings (Sydney, Melbourne) are showing compressed yields (2.8–3.4% gross) alongside moderating growth as affordability constraints bite. Meanwhile, a cohort of outer-ring capital city suburbs and regional growth corridors is delivering both above-threshold yield and above-average growth simultaneously.

The HtAG Australian Property Forecast 2026 identifies three key macro forces driving this bifurcation: sustained net overseas migration (adding approximately 260,000 persons per year to the housing demand stack), persistent undersupply of new dwellings relative to population growth (building approvals running at approximately 78% of the required replacement rate), and the lagged effect of 13 RBA rate rises between 2022 and 2024 on investor borrowing capacity. Taken together, these forces are compressing yield in premium markets while releasing pressure in affordable, high-demand corridors.

Market Condition Preferred Strategy Key Metric to Watch Red Flag Rising rates, compressed borrowing capacity Yield-first (cashflow neutrality) Net yield after costs Vacancy >2.5% Falling rates, expanding borrowing capacity Growth-first (leverage amplification) GRC phase + supply slope GRC Phase 3 (peak) Stabilising rates, recovery cycle beginning Dual-metric (yield ≥4.5% + GRC Phase 1) BA ratio + stock on market trend Yield sustained by falling prices High affordability pressure (income-to-price ratio >30 yrs) Avoid — demand ceiling limiting growth IRSAD + years-to-own ratio Flat or negative GRC despite yield

Source: HtAG Analytics, Q1 2026. Market conditions reflect current cycle phase as at April 2026. Investors should re-evaluate as conditions shift.

Data from the Suburb Growth Forecasts 2026 analysis shows that the highest-confidence suburb selections in the current environment share a specific data signature: gross yield between 4.8% and 6.4%, GRC in Phase 1 or early Phase 2, stock on market declining quarter-on-quarter, and IRSAD decile between 4 and 7 (moderate socioeconomic stability with room for upgrade). Suburbs matching all four criteria represented 7.3% of the 15,000+ suburbs tracked by HtAG Analytics as at Q1 2026 — approximately 1,100 locations nationally.

Understanding why LGA-level data is insufficient for this analysis is equally important. A single LGA may contain suburbs at very different points in the cycle — one in early recovery, another at peak. Averaging these masks the opportunity and the risk simultaneously. Suburb-level precision is non-negotiable for any data-driven investment decision.

Key Takeaways

Key Takeaways

- Rental yield and capital growth are complementary metrics, not competing strategies — the strongest investment suburbs in 2026 are delivering gross yields above 4.5% and GRC in recovery or early-growth phase simultaneously.

- A high gross yield (above 6%) with a vacancy rate above 2.5% is almost always a structural yield trap — the yield reflects stagnant or falling prices, not genuine rental demand. Filter these out before evaluating any other metric.

- According to HtAG Analytics data, 135 validated recommendations tracked on the Evidence Portal delivered a median first-year capital growth of 14.2% — outperforming the national median of 7.8% — by targeting dual-metric markets rather than single-metric extremes.

- Capital growth has a meaningful after-tax advantage over rental income for investors on marginal tax rates above 39% due to the 50% CGT discount on gains from properties held over 12 months.

- As at Q1 2026, approximately 1,100 of the 15,000+ suburbs tracked by HtAG Analytics meet the dual-metric threshold of gross yield 4.8–6.4%, GRC Phase 1–2, and vacancy below 1.5% — representing 7.3% of all tracked markets.

- Suburb-level data is essential for this analysis — LGA averages mask the cycle divergence between suburbs within the same council area and are insufficient for suburb selection.

From Data Signal to Portfolio Decision

The gross yield, GRC, vacancy rate, and IRSAD metrics described in this article are live inside the HtAG Analytics platform — updated each quarter as new valuation and rental data flows in. Professional buyers agents use these signals to filter 15,000+ suburbs down to the 30–50 candidates that genuinely merit detailed due diligence, saving hundreds of hours of manual research and dramatically improving selection accuracy.

If you’re building a portfolio and want to see the exact data powering articles like this one, the HtAG Starter Plan gives you access to suburb-level analytics across every Australian market — gross yield, GRC phase, vacancy trend, supply slope, and IRSAD score, all in one place. No lock-in, cancel any time.

Start your HtAG Analytics membership →

Frequently Asked Questions

Is rental yield or capital growth more important for property investment in Australia?

Neither metric is universally more important — the right balance depends on your investment goals, tax position, and time horizon. For investors in early portfolio-building phase needing cashflow neutrality, yield is the primary filter. For investors with equity, a long horizon, and high marginal tax rate, capital growth typically delivers better after-tax wealth outcomes. According to HtAG Analytics modelling, the highest-returning suburb selections combine gross yield above 4.5% with GRC in recovery or early-growth phase — a dual-metric approach that outperforms single-metric extremes in the majority of market conditions.

What is a good rental yield for investment property in Australia in 2026?

A good rental yield depends on the market type. In inner-city capital city markets, gross yields of 3.5–4.5% are typical and reflect strong long-term growth potential. In middle-ring and outer-ring suburbs, gross yields of 4.5–6.0% are achievable and represent the most sustainable yield range for cashflow-aware investors. Anything above 6.5% gross should be scrutinised carefully — verify the vacancy rate (must be below 1.5%) and the GRC trend before assuming the yield is sustainable. HtAG Analytics tracks gross yield across 15,000+ suburbs updated each quarter, allowing investors to compare yield in context rather than in isolation.

Which Australian suburbs offer both high yield and strong capital growth in 2026?

As at Q1 2026, the best dual-metric suburbs are concentrated in regional growth corridors across Queensland, South Australia, and Western Australia — where population growth driven by internal migration is absorbing housing stock faster than new supply can be built. Specific suburbs identified by HtAG Analytics as meeting the dual-metric threshold (gross yield 4.8–6.4%, GRC Phase 1–2, vacancy below 1.5%) are detailed in the HtAG Q1 2026 High-Yield Suburbs report. Inner-ring capital city suburbs rarely meet both criteria simultaneously in the current cycle.

How does the Growth Rate Cycle (GRC) relate to rental yield?

The Growth Rate Cycle (GRC) is a leading indicator of future capital growth, not a yield metric. However, GRC phase has indirect implications for yield: when a suburb enters GRC Phase 1 (recovery), prices typically begin rising faster than rents, which compresses yield over subsequent quarters. Buying before that compression — at the Phase 4/Phase 1 transition — captures both the yield (which is still relatively high before prices run) and the capital growth (which is beginning to accelerate). This is precisely the entry timing that HtAG Analytics’ framework is designed to identify. Learn more about the GRC at the HtAG Growth Rate Cycle explainer.

Can I use free property data to compare rental yield and capital growth across suburbs?

Free property data platforms (Domain, REA Group, Google) provide surface-level yield and median price data, but they do not provide vacancy rates, GRC phase, supply slope, or the IRSAD socioeconomic stability index — the context metrics that distinguish a genuine yield-and-growth opportunity from a yield trap. Free data is useful for initial orientation but insufficient for suburb-level investment decisions. HtAG Analytics combines all of these metrics in a single platform, updated quarterly, covering every Australian suburb tracked since 2010.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Property investment carries risks, and past performance is not indicative of future results. All growth rates, yields, and projections are derived from historical data and statistical modelling — they are not guarantees of future performance. Always conduct your own due diligence and consult a qualified financial adviser before making investment decisions.