Short Summary

Years to Own is HtAG Analytics’ housing-affordability metric — the estimated years it would take to fully repay a standard 30-year mortgage on the typical home in an area, given current house prices, current interest rates and the local median family income. On HtAG house data as at 30 June 2026 it runs from about 15 years in Kalgoorlie, WA to roughly 98 years in Mosman, NSW, and it lengthened in every market we checked over the year to June 2026 as prices and rates outpaced income growth. A reading above 30 years signals a market a typical local income can no longer comfortably buy into.

Years to Own in 30 seconds

What is it? The estimated years to fully pay off a standard 30-year mortgage on the typical home in an area, given local incomes, current interest rates and prices.

Why does it matter? It measures true affordability — whether a typical local income can actually service a typical purchase — not just the sticker price.

Who uses it? Investors gauging sustainable owner-occupier demand, buyers agents framing affordability, and homebuyers comparing markets.

Read it alone? No — pair it with the Relative Composite Score (RCS) and growth signals before acting.

If you remember one thing: above ~30 years, a typical local income can no longer comfortably buy a typical home — the higher the number, the more the market leans on wealthier buyers, investors or outside money.

Table of Contents

What is Years to Own?

Years to Own is HtAG Analytics’ housing-affordability metric: the estimated number of years it would take to fully repay a standard 30-year mortgage on the typical home in an area, based on current house prices, current interest rates and the local median family income. A reading above 30 years signals that a typical local income can no longer comfortably service a typical purchase — and the higher the number climbs, the less affordable the market.

Canonical Definition

Years to Own (Affordability Index) — the estimated duration required to fully own a property, factoring in current interest rates, median family income and typical property prices in the area, based on a standard 30-year mortgage. A value exceeding 30 years indicates decreased affordability; lower is more affordable.

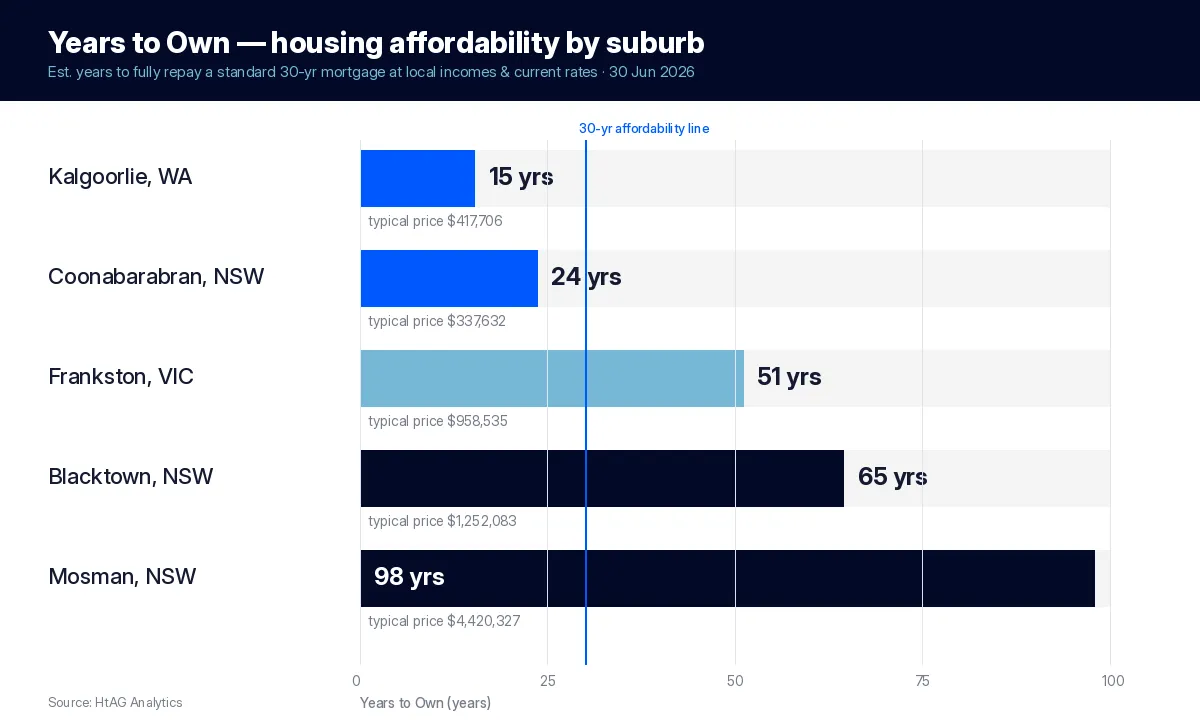

Years to Own in 2026: a snapshot

The quickest way to read Years to Own is across markets that sit at opposite ends of the affordability spectrum. According to HtAG Analytics, the metric reads about 15 years in Kalgoorlie, WA and almost 98 years in Mosman, NSW — the same metric, on the same 30-year-mortgage basis, as at 30 June 2026.

| Suburb | Typical Price | Years to Own | Affordability read |

|---|---|---|---|

| Kalgoorlie, WA | $417,706 | 15.3 | Well within the 30-year line — affordable |

| Coonabarabran, NSW | $337,632 | 23.7 | Under 30 years — affordable |

| Frankston, VIC | $958,535 | 51.1 | Well over 30 years — stretched |

| Blacktown, NSW | $1,252,083 | 64.5 | More than double the line — stretched |

| Mosman, NSW | $4,420,327 | 97.9 | Far beyond local incomes — prestige/outside money |

Source: HtAG Analytics, houses, as at 30 June 2026. Confidence: High.

According to HtAG Analytics house data as at 30 June 2026, Years to Own runs from 15.3 years in Kalgoorlie, WA to 97.9 years in Mosman, NSW — well past the 30-year mark at which a typical local income can no longer comfortably buy in.

Affordability also drifted the wrong way across the board over the last year. Every market below recorded a higher Years to Own in June 2026 than a year earlier, as prices and interest rates outpaced income growth.

How Years to Own is calculated

Years to Own combines three inputs — the typical property price, the current interest rate, and the local median family income — and expresses the result as the number of years it would take a typical household to fully repay a standard 30-year mortgage. HtAG’s published methodology assumes a household directs roughly half of its income to repayments after a 20% deposit; where the required loan outstrips what that income can service, the figure climbs well beyond 30 years.

What this means in plain English

Years to Own is an income-and-interest-rate affordability gauge, not a rent measure. It asks: if a typical local family bought the typical home today, how long would the mortgage really take to clear? Under about 30 years, ownership is realistic on local incomes; far above it, the market depends on wealthier buyers, investors or money from outside the area.

Because it is built from income and interest rates rather than rent, Years to Own is a different lens from gross rental yield (an investor’s annual income return) and from raw Typical Price. It is one of the fundamental metrics in the HtAG Data Dictionary, and it feeds HtAG’s broader Property Intelligence layer.

Housing affordability across Australia (2023 analysis)

Editor’s note (updated July 2026): the state, city and suburb analysis below is HtAG’s original 2023 study of the Years to Own metric. It remains a useful explanation of how affordability behaves through an interest-rate cycle; for current readings, use the 2026 snapshot above or any HtAG suburb dashboard.

As property prices have continued to soar across Australia in the past 3 years, prospective homebuyers are grappling with the intimidating task of affording a home. Many Australians face an overwhelming challenge when it comes to buying property in their desired area. In this comprehensive guide, we will unravel property affordability in Australia, examining the “years to own” metric as a critical component in understanding the current affordability levels across the country.

When it comes to property investment, having a thorough understanding of the market is essential for making well-informed decisions. One valuable metric to consider is the “years to own” measure, which estimates the number of years it would take to completely own a property given the current house prices, interest rates and median family income. This metric serves as a useful indicator of property affordability. In this article, we will explore the “years to own” measure in detail, examining how it varies across different property types, states cities and LGAs in Australia.

What is the “Years to Own” Metric?

The “years to own” metric is a measure of property affordability, estimating the number of years it would take for a homebuyer to fully repay their home loan. This is based on a standard 30-year mortgage term at current interest rates and median family income. The metric assumes that households contribute 50% of their wages to mortgage repayments. A higher “years to own” value indicates lower affordability, with values above 30 years signaling a concerning threshold as it suggests that borrowing capacity is exceeded.

For property investors, this metric is especially important as it provides an estimate of the time it would take for properties to be fully owned based on socioeconomics of an area.

Suburbs with high “years to own” values are likely to experience downward pressure on house prices, as locals may struggle to afford purchasing houses as prices rise and incomes lag. However, there are other market variables that may still push the prices up even in low affordability markets.

The data used for this analysis includes information on 2 property types (houses and units) across different states in Australia. Each entry in the dataset represents a specific property type within a particular local government area, accompanied by the corresponding “years to own” value.

By comparing the average “years to own” values based on state or territory, LGA, suburb and property type, we gain valuable insights into the affordability landscape across Australian markets. This information aids property investors in strategising their investments by identifying markets with lower “years to own” values that offer better affordability or potential for future growth. Furthermore, potential homebuyers can use this data to make informed decisions on where to purchase a property that best aligns with their financial goals and circumstances.

Average Years to Own by State and Property Type

One of the main discoveries from our analysis is the variation in the “years to own” metric across different states and property types.

The chart below illustrates that the average “years to own” varies considerably across states and property types. In most states, houses take longer to own on average compared to units. New South Wales stands out as the state with the highest average “years to own” for both houses and units.

Highest and Lowest “Years to Own” States: New South Wales emerges as the state with the highest average “years to own” values for both houses and units, indicating the lowest affordability. By contrast, Queensland and Northern Territory showcase the shortest “years to own” values, pointing to higher housing affordability in these regions.

Houses vs. Units: Across all states, the average time taken to own a house is consistently longer than that for a unit. This trend highlights the lower affordability of houses compared to units and the appeal of units for first-time homebuyers or individuals with limited budgets.

In states like South Australia and Queensland, the gap between owning a house and a unit is relatively smaller, indicating a more balanced property market. In contrast, Western Australia, New South Wales and Victoria exhibit a larger disparity, demonstrating the dominance of higher-priced houses in those markets.

Affordability in Relation to Surrounding States: Neighboring states can differ significantly in terms of affordability, like the case with New South Wales and Queensland. As a result, an increasing number of purchasers are considering cross-border property investment or relocation to access better affordability in a nearby state.

Least & Most Affordable Suburbs Over the Past 3 Years

To track how property affordability has evolved over time within the Australian property market, the interactive barchart below dynamically displays the least and most affordable suburbs over the past three years.

This interactive visualisation can help identify trends over time, shedding light on the factors driving these changes and providing a more comprehensive picture of the market. The barchart reveals several intriguing insights regarding the fluidity of property affordability in Australian suburbs.

Here is the description of controls to help you interact with the barchart below:

- Click on the state or territory name to exclude it

- Click on “Highest” or “Lowest” to show least affordable or most affordable suburbs

Fluctuations in Affordability Rankings: Over the course of three years, there have been notable shifts in the rankings of the least and most affordable suburbs. These changes can be attributed to a variety of factors, including regional fluctuations in housing prices, which may be driven by alterations in the supply and demand dynamics of the local housing market.

Emerging Areas of Affordability: The barchart race also highlights suburbs that have progressively become more affordable over the years. This can be attributed to a range of reasons, including increased supply, and decreasing house prices. These areas can be of particular interest to investors or homebuyers keen on identifying recovering markets with potential for capital appreciation.

The Influence of Interest Rates and Income: A crucial aspect in the “years to own” metric is the role played by interest rates and median incomes. The barchart race showcases how these factors, combined with housing prices, significantly impact the affordability of various suburbs. As interest rates rise towards 2023 and house price fall in some markets in the same period, suburbs with a higher median income may become more affordable.

Persistently Unaffordable Hotspots: Certain suburbs consistently rank as least affordable, such as those in Sydney and Melbourne, due to persistent high house prices and limited wage growth. These areas may remain out of reach for many homebuyers, limiting opportunities for property investment.

Two common factors contribute to the consistent unaffordability of suburbs with years to own above 100 — high house prices coupled with a prevalence of renters or exclusive locations with generational wealth.

High house prices coupled with a prevalence of units and renters: In these markets, a significant portion of the population is engaged in renting units rather than owning a house. While the majority of household incomes in these suburbs may suffice for renting or owning a unit, they may not be adequate for purchasing houses. This leads to a property market that primarily supports rental properties in units and maintains high house prices.

Exclusive locations with generational wealth: Prime suburbs situated near the water or in upscale locations attract a population with well-established, generational wealth. In these areas, wealth often outpaces wage and income growth for the general population. The high demand for premium real estate from affluent residents drives up prices, making it challenging for individuals with lower or average incomes to afford houses in these neighborhoods.

Over the years researched, the composition of suburbs in the top 10 least affordable markets has shifted due to various factors. As house prices rose and then fell while interest rates increased during the same period, Sydney suburbs have become more dominant in the list of least affordable markets.

For example the substantial increase in the “years to own” metric for Strathfield, from 84 to 141 years within a span of 3 years, can be attributed to several key factors:

- High house prices: Strathfield was already known for its elevated house prices, which has been a contributing factor in the area’s declining affordability.

- Staggering interest rate increases: A significant increase in interest rates during this period has driven up the cost of borrowing, making it even more challenging for potential homebuyers to afford houses in Strathfield.

- Mixed socioeconomics: Strathfield presents a mixture of socioeconomic backgrounds, where uneven income growth and disparities may exacerbate the challenge of purchasing properties for a segment of the population. While some households can support the increasing property prices and mortgage repayments, others in the same area may struggle due to financial constraints.

A 4% increase in interest rates ( from 0.1% in April 2022 to 4.1% in June 2023) has significantly impacted homeowners with home loans of above $1,000,000. As a result of this rise, their mortgage repayments could be nearly double compared to what they were paying just a year ago. This substantial increase in financial burden can strain household budgets and impact the overall affordability of homeownership in the current property market.

Sydney is home to the most expensive suburbs, and the increasing interest rates have propelled them to the forefront, outpacing Melbourne and Brisbane locations. This shift in the makeup of the suburbs highlights the varying dynamics of property affordability across the major cities, with Sydney emerging as the key area of concern in the context of housing affordability.

By understanding these trends over time, property investors and homebuyers can make better-informed decisions about where to invest and identify opportunities for potential gains.

Is the Situation Going to Get Worse for Homebuyers?

While it is impossible to determine with certainty whether the situation for homebuyers will worsen or improve, monitoring market trends, interest rates, and government policies can provide invaluable insights into the evolving housing market landscape.

The key driving forces contributing to decreasing affordability in the housing market are suggesting that the situation may get worse before improving.

Potential interest rate increases: As interest rates continue to rise, borrowing costs will increase, making it more challenging for homebuyers to enter the property market.

Continuous wage growth: While wage growth can benefit prospective homebuyers, it might also contribute to raising house prices if it outpaces affordability improvements.

Low unemployment rates: With low unemployment rates, more people have the financial capacity to purchase homes, adding further pressure on property prices.

Low listings and building approvals: A limited supply of available properties due to low listings and a decrease in building approvals can lead to heightened demand, driving up prices in the housing market.

Signs of stabilisation may appear around 2024, assuming inflation is brought under control and interest rate increases pause or reverse to more affordable levels. This change would help alleviate the pressure on housing affordability, providing relief for potential homebuyers navigating the property market.

Where Years to Own fits with HtAG’s other metrics

Years to Own is an affordability and demand-durability lens — it tells you whether local incomes can sustain a market — not a growth forecast. It works best alongside HtAG’s other suburb signals rather than on its own.

- What it is: an income-and-interest-rate affordability gauge, in years, for the typical home.

- What it is not: a rental-return figure, a capital-growth prediction, or a stand-alone buy signal. Pair it with the Relative Composite Score (RCS) and cycle reads such as Growth Pattern Deviation (GPD).

- Best used for: judging sustainable owner-occupier demand, comparing markets on the same affordability scale, and pressure-testing whether a price run has outgrown local incomes.

You can map affordability across a region with the RCS suburb heatmap, see how it interacts with deposit hurdles in our guide to how much deposit you need, or apply the same affordability thinking to a shortlist in where to invest under $500,000. Every recommendation HtAG has published is tracked in the Evidence Portal.

Surface this data inside your AI agent

The HtAG Developer Portal exposes Years to Own — and every other HtAG dataset — through MCP (Model Context Protocol) connectors. Investors and buyers agents using Claude, Perplexity, Manus AI, ChatGPT (via custom connectors) or any other MCP-compatible AI agent can query HtAG affordability data directly inside the tool they already use.

Browse the endpoint catalogue at developer.htagai.com and submit the HtAG Developer Portal application — approved members receive an API key and an MCP setup guide for their preferred AI tool.

From data signal to portfolio decision

Years to Own, RCS and the cycle metrics on this page are live inside the HtAG Analytics platform, updated as new sales, income and rate data flows in. Professional buyers agents use Years to Own to sanity-check whether a market’s price growth is supported by local incomes before committing.

Start your HtAG Analytics membership → · Apply for Developer Portal access →

Key takeaways

- Years to Own = estimated years to fully repay a standard 30-year mortgage on the typical home, from local income, interest rates and price.

- Above 30 years signals decreasing affordability; the metric can exceed 100 years in prestige markets.

- On HtAG house data at 30 June 2026 it ran from 15.3 years (Kalgoorlie, WA) to 97.9 years (Mosman, NSW).

- It worsened in every sampled market over the year to June 2026 as prices and rates outpaced incomes.

- It is an affordability lens, not rent, yield or a growth forecast — read it with RCS and cycle metrics.

Years to Own: FAQs

What does Years to Own mean?

Years to Own is HtAG Analytics’ housing-affordability metric: the estimated number of years to fully repay a standard 30-year mortgage on the typical home in an area, given current prices, interest rates and local median family income. Above 30 years indicates decreased affordability.

How is Years to Own calculated?

It combines typical price, current interest rates and median family income into the years needed to clear a standard 30-year mortgage, assuming a household directs roughly half its income to repayments after a 20% deposit. Where the required loan exceeds serviceable borrowing, the figure rises well beyond 30 years.

Is Years to Own the same as rental yield?

No. Gross rental yield measures an investor’s annual rental return; Years to Own measures owner-occupier affordability from income and interest rates. They answer different questions — a low Years to Own reflects affordable ownership, not a strong rental return.

What is a good Years to Own value?

Broadly, under 30 years suggests ownership is realistic on local incomes, while higher values signal stretched affordability. According to HtAG Analytics, it should be read with the Relative Composite Score and cycle position rather than as a stand-alone buy signal.

How do I access HtAG Years to Own data inside Claude or Perplexity?

Through the HtAG Developer Portal. Browse the catalogue at https://developer.htagai.com/ and apply at https://links.htag.com.au/widget/form/GFVegAaXzeTUH7QzRl1T. Approved members receive an API key and an MCP setup guide so any MCP-compatible AI agent can query Years to Own directly.

Citation: HtAG Analytics — Years to Own (Affordability Index). Suburb figures are houses, as at 30 June 2026 (High confidence).

The conceptual framework behind this metric is published openly for transparency and education. Its proprietary implementation — calibration, weighting, validation and the underlying data — remains the confidential intellectual property of HtAG Analytics.

Explore more: this metric is indexed in the HtAG Property Data Dictionary, and sits alongside every other concept, metric and method in the Education Hub — HtAG’s Property Intelligence Library.

This article forms part of the HtAG Property Intelligence Reference Library — a structured knowledge base documenting the concepts, metrics and methodologies used to analyse Australian residential property markets.

Reference Standard PI-YEARSTOOWN · Version 1.0

Cite this metric

HtAG Analytics defines Years to Own as: “Years to Own (the Affordability Index) is the estimated number of years to fully own a typical local home given incomes, interest rates and prices, on a standard 30-year mortgage.”

Suggested citation: HtAG Analytics, “Years to Own,” HtAG Property Data Dictionary, July 2026.

In a hypothetical scenario where there’s a 5% 𝐢𝐧𝐭𝐞𝐫𝐞𝐬𝐭 𝐫𝐚𝐭𝐞 and 𝐟𝐚𝐦𝐢𝐥𝐢𝐞𝐬 𝐚𝐫𝐞 𝐚𝐛𝐥𝐞 to dedicate 𝟓𝟎% 𝐨𝐟 𝐭𝐡𝐞𝐢𝐫 yearly income to mortgage repayments after securing a loan with a 20% deposit, it turns out that home ownership could become a reality for Aussies in just 60% of the housing markets country-wide!