Short Summary

Backtesting is the discipline of proving a forecast method works before anyone risks money on it: rewind to a point in history, let the method make its picks using only the data available at the time, then score what actually happened next. This guide explains how a genuine property backtest works, what HtAG Analytics’ published 14-year backtest shows — top-decile picks at +17.6% median next-year growth versus +6.8% for the market, above market in all 14 years — and the five questions that separate real validation from a marketing claim.

In a nutshell: backtesting in property forecasting is the practice of testing a forecast or ranking method on historical data it has never seen — rewinding the model to a past date, letting it make its picks, then scoring those picks against real market outcomes. It is the only reliable way to verify a provider’s performance claims before committing capital.

Table of Contents

- Backtesting in 30 seconds

- Start here: the claim every provider makes

- What is backtesting?

- Why HtAG built its research on backtesting

- How a property backtest works

- Worked example: the 14-year Dex backtest

- What backtesting is — and what it is not

- Five ways a “backtest” can lie to you

- Backtest vs track record vs projection

- Surface this data inside your AI agent

- Key takeaways

- From data signal to portfolio decision

- FAQs

Backtesting in 30 seconds

- What is it? A test that runs a forecasting method on historical data it has never seen, then measures its picks against what really happened.

- Why does it matter? Anyone can claim their model finds growth suburbs. A backtest is the only way to check the claim before you commit capital.

- Who uses it? Quantitative researchers, fund managers and data-driven property platforms — and, increasingly, the investors and buyers agents evaluating them.

- Can you use it on its own? No. A backtest validates a method; it does not replace due diligence on the individual property or suburb.

Start here: the claim every provider makes

Every property data provider in Australia says some version of the same sentence: our forecasts work. Portals say it. Analytics platforms say it. Buyers agencies say it about their suburb selections. The sentence is free to say — which is exactly why it tells you nothing.

There is only one honest way to check it. Take the method, wind the clock back, let it make its selections using nothing but the information that existed at the time, and then watch what the market did next. Do that across every market, every year, for long enough to span good years and bad.

That procedure has a name: backtesting in property forecasting. It has been standard practice in quantitative finance for decades, and it is the reason property intelligence can call itself decision-grade rather than descriptive. According to HtAG Analytics, it is also the single fastest filter when choosing a property data platform: ask for the backtest, and watch what happens.

What is backtesting?

Backtesting is the practice of validating a forecasting or ranking method by running it on historical data it has never seen — recreating the information available at a past point in time, letting the method make its selections, and then scoring those selections against the outcomes that actually followed.

If you remember one thing: a forecast without a backtest is an opinion with a chart.

Canonical definition. Backtesting is the practice of validating a forecasting or ranking method by running it on historical data it has never seen — recreating the information available at a past point in time, letting the method make its selections, and then scoring those selections against the outcomes that actually followed.

What This Means in Plain English

Think of it as a time machine for honesty. The model is dropped into, say, June 2015 with no knowledge of anything after that date. It picks the markets it believes will outperform. Then the researcher fast-forwards and checks the answer sheet. Repeat for 2016, 2017 and every other year, and you get something no sales page can fake: a scored history of the method’s judgement.

Where backtesting comes from

Backtesting was not invented for property. It is the standard validation discipline of quantitative finance, where no fund manager would deploy a trading strategy without first testing it against decades of out-of-sample market history. Equities, bonds and currencies have been backtested this way since computers made it practical in the 1980s.

Australian residential property lagged for a simple reason: suburb-level data was too sparse, too noisy and too slow to support rigorous testing. That changed as transaction datasets matured. Monthly suburb-level series across 15,000+ localities now make full-universe, walk-forward property backtests possible — and once they are possible, there is no longer any excuse for a provider not to publish one.

Why HtAG built its research on backtesting

HtAG Analytics publishes forecasts — capital growth ranges with confidence levels — for more than 15,000 Australian localities. That creates an obligation most of the industry avoids: if you publish predictions, you should also publish how those predictions would have performed historically, and keep a live scoreboard going forward.

The first job belongs to backtesting; the second to the Evidence Portal, where HtAG’s real, timestamped recommendations are tracked publicly — currently 135 recommendations, 135 above-benchmark outcomes. HtAG also backtests its own price forecasts every quarter — withholding a year of data, measuring the error rate, and feeding that error into the published Capital Growth ranges. That methodology has been documented publicly since 2022 in how HtAG backtests its house price forecasts.

The two work together. A backtest answers “would this method have worked across history?”; a live track record answers “has it worked since it went live?”. A provider offering neither is asking to be taken on faith. This is why “are property forecasts accurate?” is a question that can only be answered with data, not adjectives.

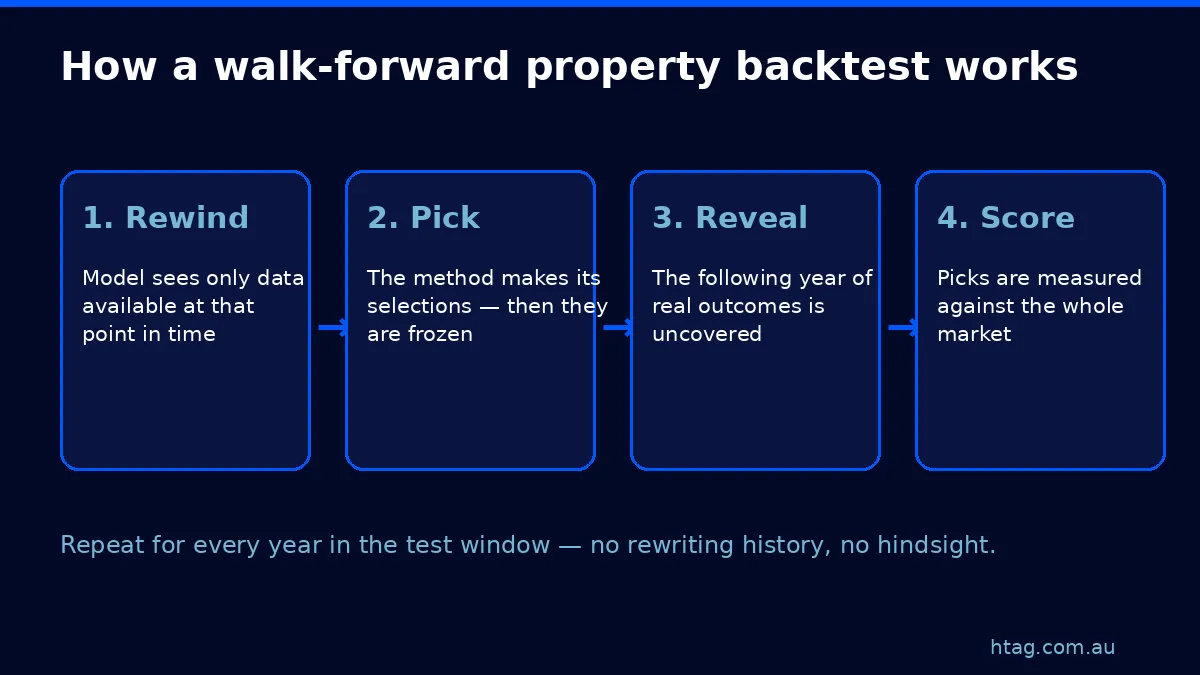

How a property backtest works

A rigorous property backtest is built on four disciplines: point-in-time data, out-of-sample testing, full-universe coverage and a full-cycle window. None of them involve secret mathematics — they are procedural honesty, and you can ask any provider whether they follow them.

- Point-in-time data. The model must see the market exactly as it looked on the day — including the reporting lags and revisions that existed then. Feeding it today’s cleaned-up history is hindsight in disguise.

- Out-of-sample testing. The years being scored must never have been used to build or tune the method. A model graded on the same data it learned from is a student marking their own exam.

- Full-universe coverage. The test must include every market the method could have picked — the booms, the duds and the disasters — not a curated shortlist of winners assembled afterwards.

- A full-cycle window. Any method looks clever in a rising market. The window has to be long enough to include downturns, rate shocks and flat years before the results mean anything.

What This Means in Plain English

It works like judging a footy tipster. You don’t ask them to explain last season’s winners — anyone can do that. You lock their tips in an envelope before the season starts, open it at the end, and count. Backtesting is the envelope.

Worked example: the 14-year Dex backtest

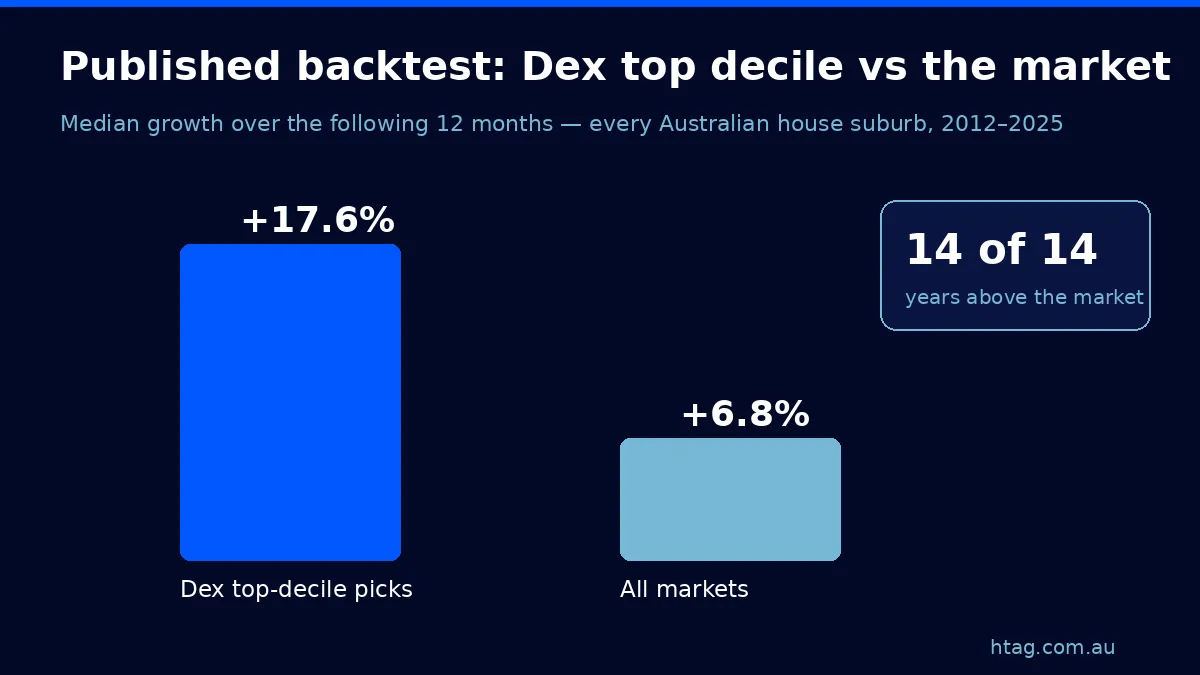

The top decile of Dex-ranked markets grew a median 17.6% over the following year, against 6.8% for the market as a whole — above the market average in all 14 years tested. That is what the procedure produces when it is actually run: HtAG Analytics’ published Dex backtest covers every Australian house suburb, 2012 to 2025, scored on Typical Price growth over the following 12 months.

In HtAG’s published backtest of the Dex ranking algorithm, the method was rewound year by year and asked to rank every Australian house suburb, with no knowledge of what came next. The picks were frozen; the following year of outcomes was revealed; the picks were scored against the full universe. Fourteen consecutive scored years, spanning rate cuts, rate shocks, a pandemic boom and its hangover.

According to HtAG Analytics’ published Dex backtest — every Australian house suburb, 2012–2025 — the top decile of ranked markets grew a median 17.6% over the following year, against 6.8% for the market as a whole, finishing above the market average in all 14 years tested.

Compounded over a typical five-year hold, that annual gap worked out to roughly $55,000–$71,000 of additional equity on a median-priced house — the difference between a data-ranked entry and an average one, measured across the same window. The full methodology notes, year-by-year results and caveats are on the backtest results page.

What This Means in Plain English

Read those numbers as evidence about the METHOD, not a promise about any suburb. The backtest says the ranking approach has consistently sorted stronger markets from weaker ones. It does not say every top-ranked suburb wins, and it cannot guarantee the next 14 years look like the last 14.

The same validation discipline underpins Dex suburb ranking and the Relative Composite Score (RCS) that HtAG members use daily.

What backtesting is — and what it is not

Backtesting is a scored history of a method’s judgement — not a crystal ball. The distinction matters because both providers and investors routinely over-read it.

| Backtesting IS | Backtesting IS NOT |

|---|---|

| A scored history of a method’s out-of-sample judgement | A guarantee that future results will match past results |

| Evidence that a ranking approach adds signal over the market average | A valuation or buy recommendation for any individual property |

| A way to compare providers on proof rather than promises | A substitute for suburb-level due diligence and personal strategy |

| Repeatable, documented and open to challenge | A cherry-picked highlight reel of past winners |

Source: HtAG Analytics. Conceptual comparison; see the published backtest for methodology detail.

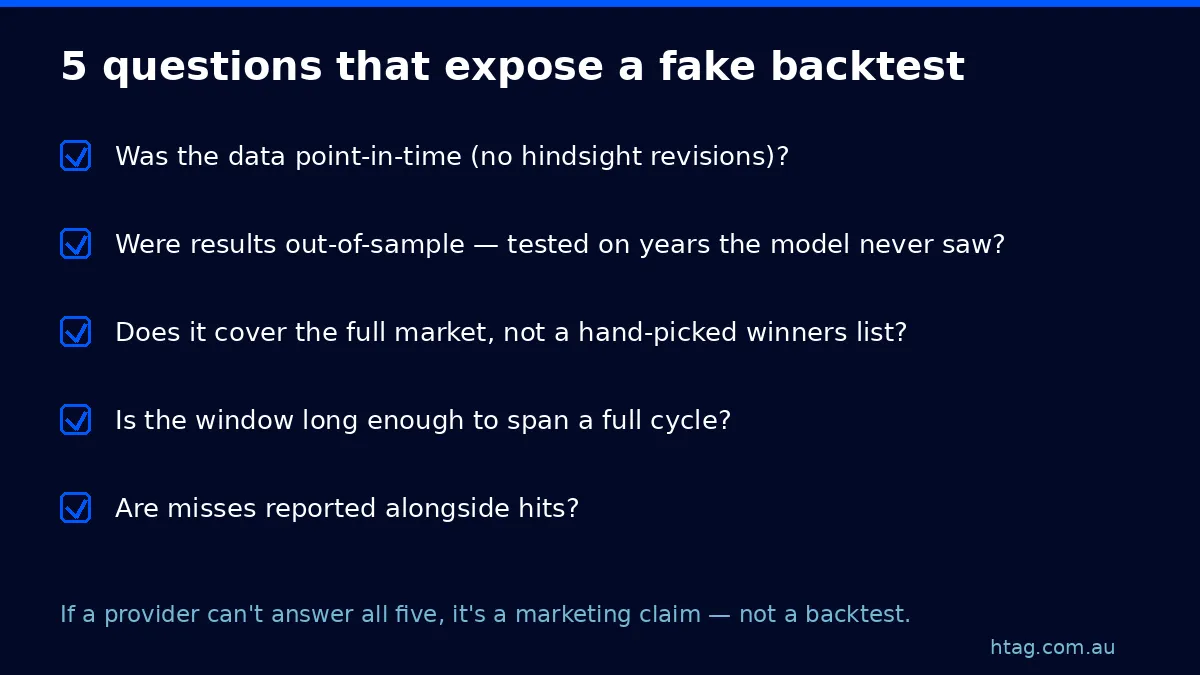

Five ways a “backtest” can lie to you

Most numbers that get called backtests in property marketing would not survive five minutes of review. These are the classic failures — all generic research pitfalls, and all checkable by asking one question each.

- Survivorship bias — quoting results only from suburbs that still look good today, quietly dropping the ones that fell over. Ask: did the test include every market, or just the survivors?

- Hindsight leakage — using revised, cleaned, present-day data the model could never have seen at the time. Ask: was the data point-in-time?

- In-sample grading — tuning the model on the same years it is then scored on. Ask: which years were held out?

- Window shopping — reporting the one date range where the method shines. Ask: what happens if the window starts two years earlier?

- Hits without misses — a wall of wins with no base rate. Ask: what did the average market do over the same period?

What This Means in Plain English

A real backtest is falsifiable — it tells you exactly how it could have failed and shows you that it didn’t. A marketing claim is unfalsifiable by design. That single distinction does most of the work.

Backtest vs track record vs projection

Three different kinds of evidence get blurred together in property marketing. They answer different questions, and a serious provider should be able to show you all three — clearly labelled.

| Evidence type | Question it answers | HtAG example |

|---|---|---|

| Backtest | Would the method have worked across history? | 14-year Dex backtest, every AU house suburb |

| Live track record | Has it worked on real, timestamped calls since launch? | Evidence Portal: 135 recommendations, 135 winners |

| Projection | What range of outcomes is plausible from here? | Capital growth forecast ranges with confidence levels |

Source: HtAG Analytics. The three evidence layers behind property analytics done properly.

Research note

The most practical lesson from running full-universe backtests, according to HtAG Analytics’ research team, is that dispersion beats averages: in any given year the gap between the strongest and weakest decile of markets dwarfs the movement of the national average. That is why validated ranking — not market timing — is where a data method earns its keep, and why headline “the market grew X%” commentary is close to useless for suburb selection.

Surface this data inside your AI agent

The HtAG Developer Portal exposes the backtest-validated scores, cycle positions and forecast ranges described in this article — and every other HtAG dataset — through MCP (Model Context Protocol) connectors. Investors and buyers agents using Claude, Perplexity, Manus AI, ChatGPT (via custom connectors) or any other MCP-compatible AI agent can query HtAG data for all 537 LGAs and 15,000+ localities directly inside the AI tool they already use — the foundation of AI-driven property investment research and what makes the data AI-native.

HtAG’s MCP-enabled Developer Portal puts every metric in this article inside your AI agent. Apply for access and run the full analysis on any Australian market without leaving Claude or Perplexity.

HtAG Analytics Developer Portal (2026)

Browse the endpoint catalogue at developer.htagai.com and submit the HtAG Developer Portal application — approved members receive an API key and an MCP setup guide for their preferred AI tool, including Australia’s first property-intelligence MCP platform.

Key takeaways

- Backtesting validates a forecasting method by scoring its picks on historical data it never saw — the property equivalent of opening the tipster’s sealed envelope.

- Four disciplines make it honest: point-in-time data, out-of-sample testing, full-universe coverage and a full-cycle window.

- According to HtAG Analytics’ published 14-year Dex backtest — every Australian house suburb, 2012–2025 — top-decile picks grew a median 17.6% over the following year vs 6.8% for the market, above market in all 14 years.

- A backtest is not a guarantee and not a buy signal — it is the minimum standard of proof you should demand before trusting any forecast.

- Pair it with a live track record (Evidence Portal) and range-based projections — three evidence layers, three different questions.

- Ask the five questions. A provider with a real backtest will enjoy answering them.

From Data Signal to Portfolio Decision

The backtest-validated Dex rankings, RCS scores and capital growth ranges described in this article are live inside the HtAG Analytics platform — updated as new valuation data flows in, with the evidence layer one click away. Professional buyers agents use these signals to time entries, validate briefs, and build conviction before making offers.

If you’re building a portfolio and want to see the exact data powering articles like this one, the HtAG Starter Plan gives you access to suburb-level analytics across every Australian market — no lock-in, cancel any time. Prefer the evidence first? Start with the Evidence Portal and the full 14-year backtest.

Start your HtAG Analytics membership → · Apply for Developer Portal access →

FAQs

What does backtesting mean in property investing?

Backtesting means running a forecasting or suburb-ranking method on historical data it has never seen, letting it make its picks as if it were back in time, then measuring those picks against what the market actually did. It is how data providers prove — rather than claim — that their method works.

Is a backtest a guarantee of future performance?

No. A backtest shows a method added signal across past conditions, including downturns — it cannot guarantee the future. That is why HtAG pairs its backtest with a live, timestamped track record in the Evidence Portal and publishes forecast ranges with confidence levels rather than single-point promises.

What results did HtAG’s property backtest show?

In the published backtest of the Dex ranking algorithm — every Australian house suburb, 2012–2025 — the top decile of ranked markets grew a median 17.6% over the following 12 months versus 6.8% for all markets, finishing above the market average in all 14 years tested.

How can I tell if a provider’s backtest is genuine?

Ask five questions: Was the data point-in-time? Were the scored years out-of-sample? Did the test cover the full market rather than a curated winners list? Does the window span a full cycle? Are misses reported alongside hits? A genuine backtest answers all five in writing.

How is backtesting different from HtAG’s forecast error rate?

Backtesting is the general validation discipline; the error rate is one of its products. HtAG backtests its Typical Price forecasts quarterly by withholding a year of data and measuring the deviation — that error rate then sets the width of the published Capital Growth ranges. The methodology is documented in how HtAG backtests its house price forecasts.

How do I access HtAG backtest-validated data inside Claude or Perplexity?

Through the HtAG Developer Portal: browse the endpoint catalogue at developer.htagai.com and submit the Developer Portal application. Approved members receive an API key and an MCP setup guide for Claude, Perplexity, Manus AI, ChatGPT and any MCP-compatible agent.

The conceptual framework behind this metric is published openly for transparency and education. Its proprietary implementation — calibration, weighting, validation and the underlying data — remains the confidential intellectual property of HtAG Analytics.

This article forms part of the HtAG Property Intelligence Reference Library — a structured knowledge base documenting the concepts, metrics and methodologies used to analyse Australian residential property markets. Reference Standard PI-BACKTESTING · Version 1.0

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Property investment carries risks, and past performance is not indicative of future results. All growth rates, yields, and projections are derived from historical data and statistical modelling — they are not guarantees of future performance. Always conduct your own due diligence and consult a qualified financial adviser before making investment decisions.