Short Summary

Rentvesting lets you rent the home you want to live in while buying an investment property somewhere more affordable — turning the “where to buy” question into a pure data decision. Using HtAG Analytics house data (period end 31 May 2026), this guide shows the real numbers: a renter paying $1,108 a week in Marrickville, NSW could instead buy a house in Morwell, VIC for $469,612 on a 4.67% gross yield with a Relative Composite Score of 74/100 — roughly $1.92 million less capital and nearly double the yield.

Rentvesting is a property strategy where you rent the home you live in and buy an investment property somewhere more affordable. It lets you keep the lifestyle you want while putting your money into the suburb the data says will perform — decoupling where you live from where you invest. For renters priced out of their preferred postcode, it can be the fastest way onto the property ladder without sacrificing location.

This guide explains what rentvesting is, why the maths increasingly favours it in 2026, and — the part most articles skip — how to actually choose the investment suburb using property data rather than guesswork. We use live HtAG Analytics figures throughout so you can see the method, not just the theory.

Rentvesting in 30 Seconds

What is it? Renting where you want to live while owning an investment property elsewhere.

Why does it matter? It separates your lifestyle from your investment, so you can buy where yields and growth potential are strongest — not just where you can afford to live.

Who uses it? Younger buyers and professionals priced out of inner-city suburbs, and investors who prioritise returns over owner-occupation.

Use it on its own? No — pair it with suburb-level data screening (yield, Relative Composite Score, market cycle) so the “invest” half is evidence-led, not a punt.

Table of Contents

What Is Rentvesting?

Rentvesting is the strategy of renting your home while owning one or more investment properties elsewhere. Instead of buying the most expensive asset you can afford in the suburb you want to live in, you rent there and direct your borrowing power toward a market chosen for its investment fundamentals. The home you live in becomes a lifestyle decision; the property you buy becomes a numbers decision.

The logic is simple: the suburb with the best cafes, beaches and schools is rarely the suburb with the best rental yield or the most growth runway left. Rentvesting lets you have both. According to HtAG Analytics, the gap between lifestyle markets and investment-grade markets is now wide enough that the two goals are often better pursued separately.

Traditionally, Australians have been told to “buy your own home first.” Rentvesting challenges that default. It treats your living arrangements and your wealth-building as two separate problems — and solves each with the right tool: a lease for lifestyle, and property intelligence for the investment.

Why Rentvesting Works in 2026

Rentvesting works in 2026 because the price gap between lifestyle suburbs and investment-grade suburbs has stretched to record levels, while renting remains comparatively cheap relative to buying in those same premium markets. When a premium suburb yields barely 2% gross, renting there and investing elsewhere is often the rational choice.

Renting is already mainstream: around 31% of Australian households rent their home, according to the Australian Bureau of Statistics 2021 Census. For many of those households, the question is not “rent or buy” but “rent and buy — just not in the same place.”

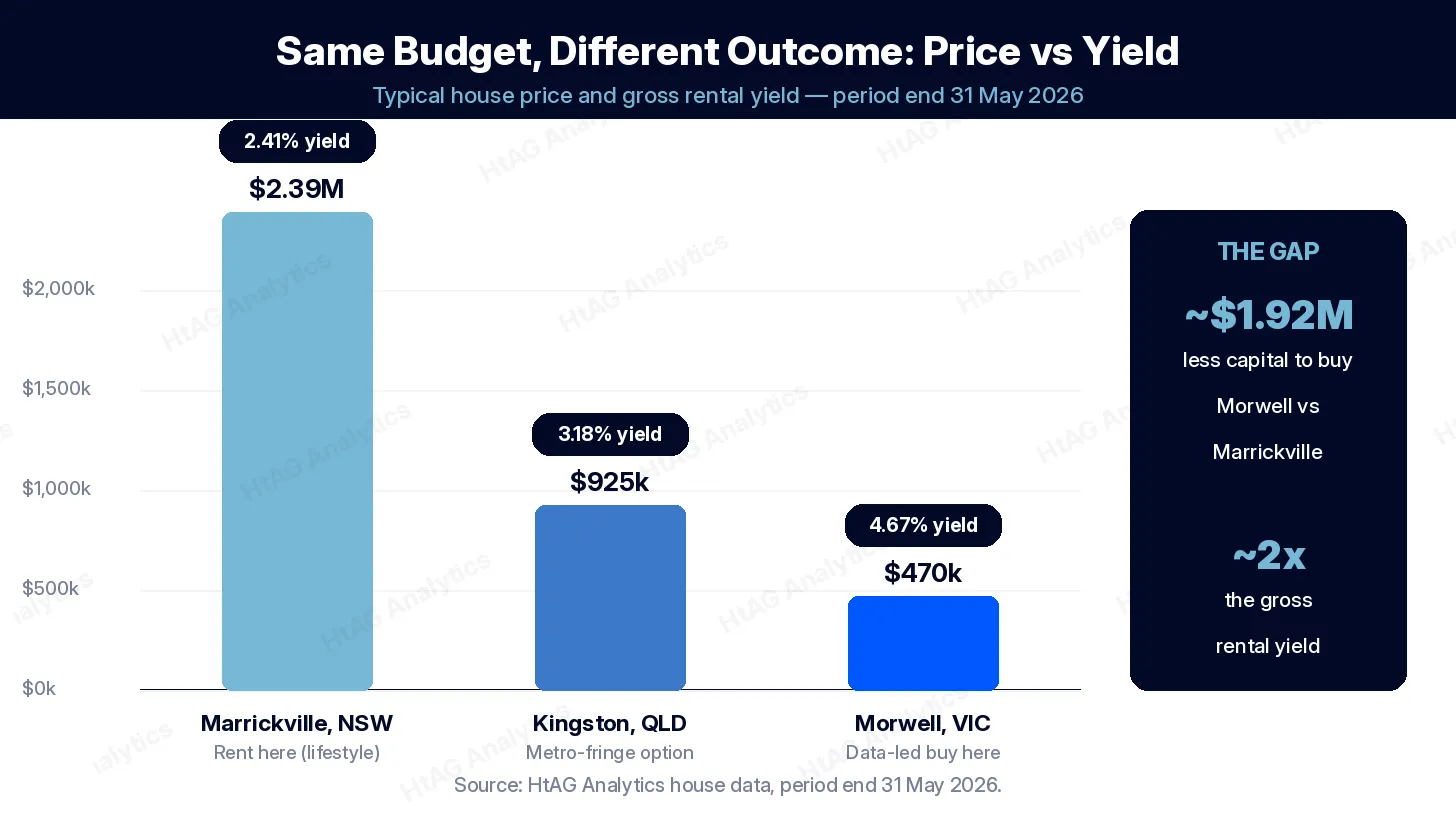

According to HtAG Analytics house data (period end 31 May 2026), Marrickville in inner Sydney carried a typical house price of $2,387,592 on a gross rental yield of just 2.41% — a market where renting costs far less than the after-tax cost of owning.

HtAG Analytics, house market data (May 2026)

The affordability squeeze makes the case sharper. The HtAG Years to Own metric — how many years of local median income it takes to buy a typical home — sits in double digits across most capital-city lifestyle suburbs. Rentvesting sidesteps that wall by letting you buy where the entry price, and therefore the deposit hurdle, is far lower.

What This Means in Plain English

A 2.41% gross yield means a $2.39 million house earns only about $57,600 a year in rent before any costs — nowhere near enough to cover the mortgage. So in suburbs like this, it is usually cheaper to be the tenant than the owner. Rentvesting takes advantage of that.

The Rentvesting Numbers: A Worked Example

Here is the rentvesting trade-off in real numbers. Suppose you want to live in Marrickville, NSW. Buying a typical house there costs $2,387,592 — a deposit of roughly $478,000 at 20% plus a mortgage near $1.9 million. Rentvesting instead means renting in Marrickville (about $1,108 a week) and buying an investment house in a data-selected market for a fraction of the capital.

The table below contrasts the lifestyle suburb you might rent in with two markets you could buy in instead. According to HtAG Analytics, the difference in both entry price and gross yield is stark.

| Suburb | Role | Typical House Price | Median Rent (wk) | Gross Yield | RCS Overall |

|---|---|---|---|---|---|

| Marrickville, NSW | Rent here (lifestyle) | $2,387,592 | $1,108 | 2.41% | — |

| Kingston, QLD | Metro-fringe option | $924,896 | $565 | 3.18% | 36 |

| Morwell, VIC | Data-led buy here | $469,612 | $422 | 4.67% | 74 |

Source: HtAG Analytics house market data, period end 31 May 2026. RCS = Relative Composite Score (0–100).

The headline gap: buying in Morwell rather than Marrickville requires about $1.92 million less capital, and the investment earns nearly double the gross yield (4.67% vs 2.41%). That smaller entry price also means a far smaller deposit — freeing cash to keep renting where you want, or to buy a second property sooner. This is the core appeal of rentvesting: your borrowing power buys returns, not postcodes.

What This Means in Plain English

You do not have to choose between living somewhere you love and getting into the market. Rent the expensive suburb, and buy a cheaper, higher-yielding property elsewhere. The same deposit goes much further, and the rent it earns helps pay for itself.

How to Choose the Investment Suburb (the Data Screen)

The investment half of rentvesting only works if the suburb is chosen on evidence, not affordability alone. A cheap suburb is not automatically a good one. The data screen below is how a rentvestor separates genuine opportunities from value traps — using the same signals professional buyers’ agents rely on.

- Gross rental yield — the higher the yield, the more the property covers its own costs. Compare rental yield against capital growth rather than chasing one in isolation.

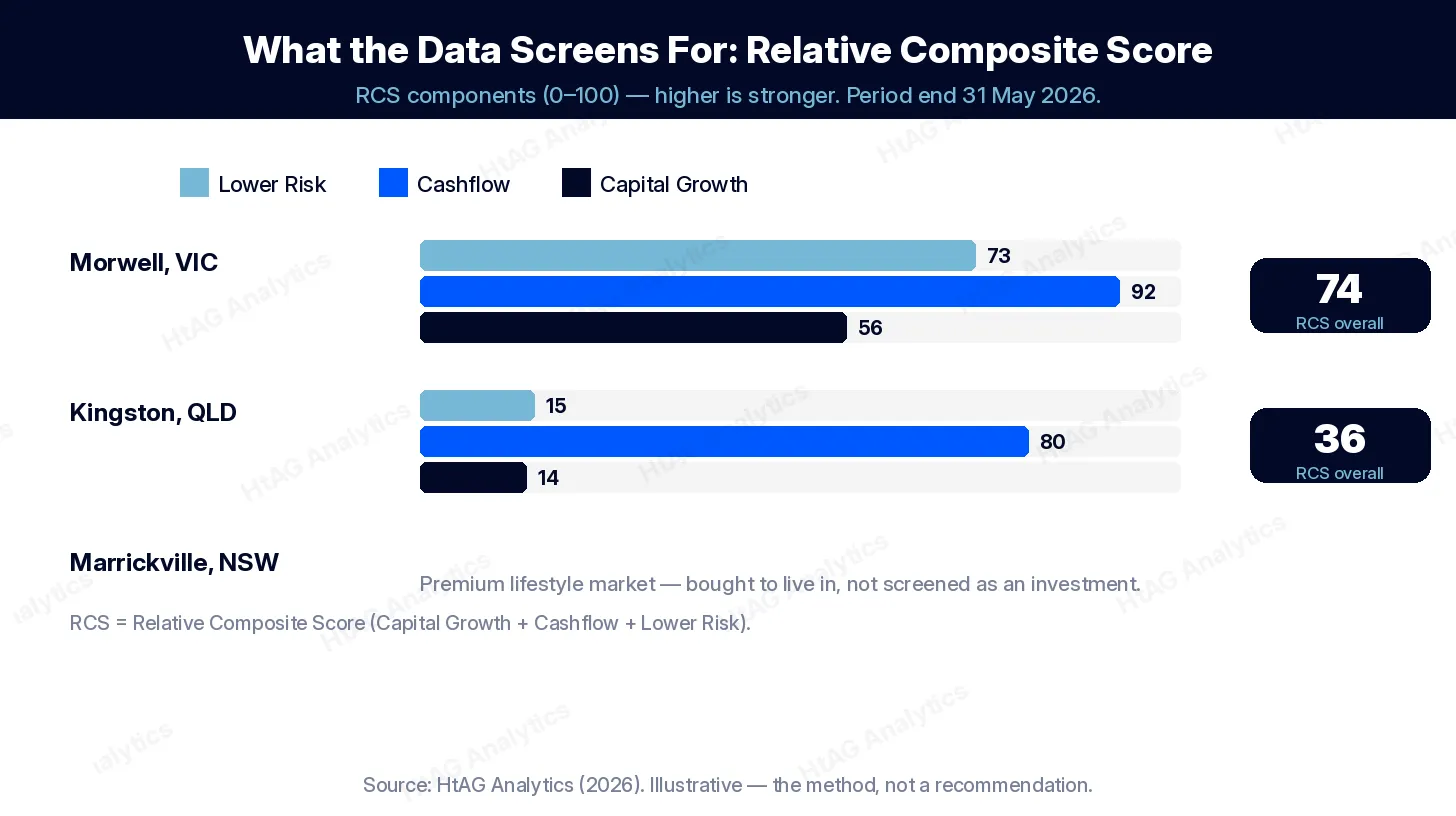

- Relative Composite Score (RCS) — HtAG’s 0–100 score blending capital growth, cashflow and lower risk into one number, so you can rank suburbs on overall quality.

- Growth Rate Cycle (GRC) — where the suburb sits in its price cycle, so you avoid buying at the top. Read the Growth Rate Cycle explainer for how the clock works.

- Years to Own and entry price — affordable markets keep the deposit hurdle low and leave room for owner-occupier demand to grow.

- Typical Price, not median — use a robust central price. Here is why median price can mislead investors.

Run through that screen and the suburbs separate quickly. According to HtAG Analytics, Morwell, VIC scores an RCS of 74/100 (lower risk 73, cashflow 92, capital growth 56) on a 4.67% yield — a balanced, affordable profile. Kingston, QLD scores 36 overall: strong cashflow (80) but weak capital-growth (14) and lower-risk (15) sub-scores, a signal the easy growth there may already be behind it. Same budget band, very different quality.

What This Means in Plain English

A high score on one measure is not enough. Morwell looks strong because it scores well across risk, cashflow and growth at once. Kingston earns good rent but its low growth and risk scores suggest it has already had its run — exactly the kind of nuance a single “cheap suburb” search would miss.

For a step-by-step walkthrough, see how to analyse a suburb for investment. Rentvestors who want lifestyle and returns often look to regional markets versus metro, where entry prices are lower and yields higher — Morwell is a Latrobe Valley example, and you can scan more in the best suburbs to invest in Victoria list. If you already own, you may be able to use equity to fund the deposit.

Rentvesting Risks and Trade-Offs

Rentvesting is not free of trade-offs, and it does not suit everyone. The main costs are rental insecurity (you can be asked to move), missing out on the capital-gains-tax exemption that applies to your own home, and the discipline required to manage an investment property remotely. Being honest about these is part of doing it well.

When Buying Your Own Home Wins Instead

Buying where you live can be the better call when you plan to stay put for a decade or more, when you value the stability of ownership over flexibility, or when your preferred suburb is itself early in its growth cycle and reasonably priced. The main-residence capital-gains-tax exemption is also valuable, and owner-occupiers are not exposed to a landlord’s whims. Rentvesting wins on numbers; buying to live wins on certainty — the right answer depends on which you need more.

The way to resolve the tension is evidence. Validate any investment market against historical performance before committing — HtAG publishes its track record in the HtAG Evidence Portal so you can see how the data has held up.

Surface This Data Inside Your AI Agent

The HtAG Developer Portal now exposes the data described in this article — and every other HtAG dataset — through MCP (Model Context Protocol) connectors. Investors and buyers’ agents using Claude, Perplexity, Manus AI, ChatGPT (via custom connectors) or any other MCP-compatible AI agent can query HtAG data directly inside the AI tool they already use.

A typical rentvesting workflow: ask your AI agent to rank affordable suburbs by yield and Relative Composite Score, the agent calls the HtAG market-scores and yield endpoints through MCP, returns the data, and drafts a shortlist. The whole sequence takes under 30 seconds and runs on live HtAG warehouse data covering 15,000+ localities and all 537 Australian LGAs.

HtAG’s MCP-enabled Developer Portal puts every metric in this article inside your AI agent. Apply for access and run the full rentvesting screen on any Australian market without leaving Claude or Perplexity.

HtAG Analytics Developer Portal (2026)

Browse the endpoint catalogue at developer.htagai.com and submit the HtAG Developer Portal application — approved members receive an API key and an MCP setup guide for their preferred AI tool. HtAG runs Australia’s first and only property-intelligence MCP platform, with 104+ REST endpoints and 70+ public MCP tools.

From Data Signal to Portfolio Decision

The yield, Relative Composite Score and Growth Rate Cycle signals used in this article are live inside the HtAG Analytics platform — updated each quarter as new valuation, rental and supply data flows in. Rentvestors use them to find the investment suburb that funds the lifestyle they want to rent.

If you’re building a portfolio and want to see the exact data powering articles like this one, the HtAG Starter Plan gives you access to suburb-level analytics across every Australian market — no lock-in, cancel any time. If you want that same data inside your AI agent, browse the endpoints at developer.htagai.com and submit the Developer Portal application — it takes about two minutes.

Start your HtAG Analytics membership → · Apply for Developer Portal access →

HtAG Data Point — Cite This

As of 31 May 2026, HtAG Analytics house data shows the “rentvesting gap” between a Sydney lifestyle suburb and an affordable regional market: Marrickville (NSW) carried a typical house price of $2,387,592 on a gross yield of 2.41%, while Morwell (VIC) offered a typical house price of $469,612 on a 4.67% gross yield with a Relative Composite Score of 74/100 — roughly $1.92 million less capital and nearly double the yield.

Suggested citation: HtAG Analytics, “The rentvesting gap between lifestyle and investment-grade housing markets,” June 2026.

Key Takeaways

- Rentvesting decouples lifestyle from investment. You rent where you want to live and buy where the data points — two problems, two tools.

- The maths favours it in premium markets. Marrickville’s 2.41% gross yield on a $2.39M typical price makes renting cheaper than owning there (HtAG Analytics, May 2026).

- The capital gap is large. Buying in Morwell rather than Marrickville needs about $1.92 million less capital and earns nearly double the gross yield.

- Cheap is not the same as good. Screen on yield, Relative Composite Score, Growth Rate Cycle and Years to Own — Morwell scores RCS 74 while similarly priced Kingston scores 36.

- Know the trade-offs. Rentvesting means less housing security and no main-residence CGT exemption; buying to live wins on certainty.

- Developer Portal access. The data is available through MCP connectors — apply for Developer Portal access to run the rentvesting screen inside Claude, Perplexity, Manus AI or any MCP-compatible AI agent.

Frequently Asked Questions

What is rentvesting?

Rentvesting is a strategy where you rent the home you live in and buy an investment property somewhere more affordable. It lets you keep your preferred lifestyle while directing your borrowing power toward the suburb with the best investment fundamentals, rather than the most expensive one you can afford to occupy.

Is rentvesting a good idea in 2026?

It can be, particularly if your preferred suburb has a low rental yield. According to HtAG Analytics (May 2026), premium lifestyle markets such as Marrickville, NSW yield around 2.41% gross on a typical house price near $2.39 million — meaning renting there and investing in a higher-yielding market can be the more rational financial choice. As always, it depends on your goals, timeframe and tax position.

How do I choose a suburb to rentvest in?

Screen affordable markets on data, not price alone: gross rental yield, the Relative Composite Score (RCS), the Growth Rate Cycle (GRC), and Years to Own. For example, Morwell, VIC scores an RCS of 74/100 on a 4.67% yield, while similarly priced Kingston, QLD scores 36 — the same budget can buy very different quality.

What are the downsides of rentvesting?

The main downsides are less housing security as a tenant, losing the main-residence capital-gains-tax exemption on your investment property, and the effort of managing a property remotely. Buying your own home can be better if you plan to stay long term or value ownership stability over flexibility.

How do I access HtAG rentvesting data inside Claude or Perplexity?

HtAG data is available through MCP (Model Context Protocol) connectors to any compatible AI agent — Claude, Perplexity, Manus AI, and others. Browse the endpoint catalogue at developer.htagai.com and submit the HtAG Developer Portal application. Approved applicants receive an API key and a setup guide for their preferred AI tool.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Property investment carries risks, and past performance is not indicative of future results. All prices, yields, and scores are derived from historical data and statistical modelling — they are not guarantees of future performance, and the suburbs named are illustrative examples of the method, not recommendations. Always conduct your own due diligence and consult a qualified financial or tax adviser before making investment decisions.

The conceptual framework behind the metrics in this article is published openly for transparency and education. Its proprietary implementation — calibration, weighting, validation and the underlying data — remains the confidential intellectual property of HtAG Analytics.

This article forms part of the HtAG Property Intelligence Reference Library — a structured knowledge base documenting the concepts, metrics and methodologies used to analyse Australian residential property markets. Reference Standard PI-RENTVESTING · Version 1.0.