Short Summary

We tracked every sizeable Australian house market through the five years after the 2021 boom. The suburbs that boomed hardest went on to grow a median 34.0% – the coolest tenth grew 62.4%. Yet after the 2014 boom, the exact opposite happened. One hot year, on its own, tells you almost nothing about the next five.

In 30 Seconds

What is this? A two-cohort HtAG study of what happens to a suburb’s prices in the five years after a boom year.

Why does it matter? “It just boomed” is the most common reason people buy – and the least reliable.

Who uses it? Investors and buyers agents deciding whether to follow heat or fade it.

Can you use recent growth on its own? No. In 2021 it cost you ~28 percentage points; in 2014 it paid. Cycle position decides which regime you are in.

Every boom ends with the same question. A suburb has just put on 30% in a year, the headlines are breathless, and buyers want to know: is that momentum, or is that the top?

What happens after a property boom is measurable: across 3,886 Australian house markets, suburbs in the hottest tenth of the 2021 boom grew a median 34.0% over the next five years, while the coolest tenth grew 62.4%. But after the 2014 boom the hottest tenth kept winning. The answer is regime-dependent – and that is the finding.

Table of Contents

- How We Tested It: 3,886 Suburbs, Five Years

- The Boom-Chaser Penalty in the 2021 Cohort

- Byron Bay vs Armadale: The Reversal in Two Suburbs

- When Chasing Heat Worked: The 2014 Cohort

- Why One Hot Year Tells You So Little

- What This Means If You’re Buying in 2026

- Surface This Data Inside Your AI Agent

- Key Takeaways

- From Data Signal to Portfolio Decision

- Frequently Asked Questions

How We Tested It: 3,886 Suburbs, Five Years

We took every Australian house market in the HtAG warehouse with a Typical Price reading in June 2020, June 2021 and May 2026, and at least 30 house sales in the boom year to June 2021 – 3,886 markets in total. Each suburb was ranked by its price growth in that boom year and grouped into ten equal deciles, from coolest to hottest. Then we measured what each decile did over the following five years.

This is the same warehouse that powers HtAG’s 14-year algorithm backtest and the recent boom contagion study. No forecasts are involved – every number below is realised history. To keep the test honest, we repeated the whole exercise on an earlier boom: the 3,591 markets with at least 30 sales in the year to June 2014, tracked to June 2019.

What This Means in Plain English

Think of it as lining up every suburb in the country by how hard it boomed, then coming back five years later to see who actually got rich. We did it twice – once for the 2021 boom, once for the 2014 one – so a single lucky era could not dictate the answer.

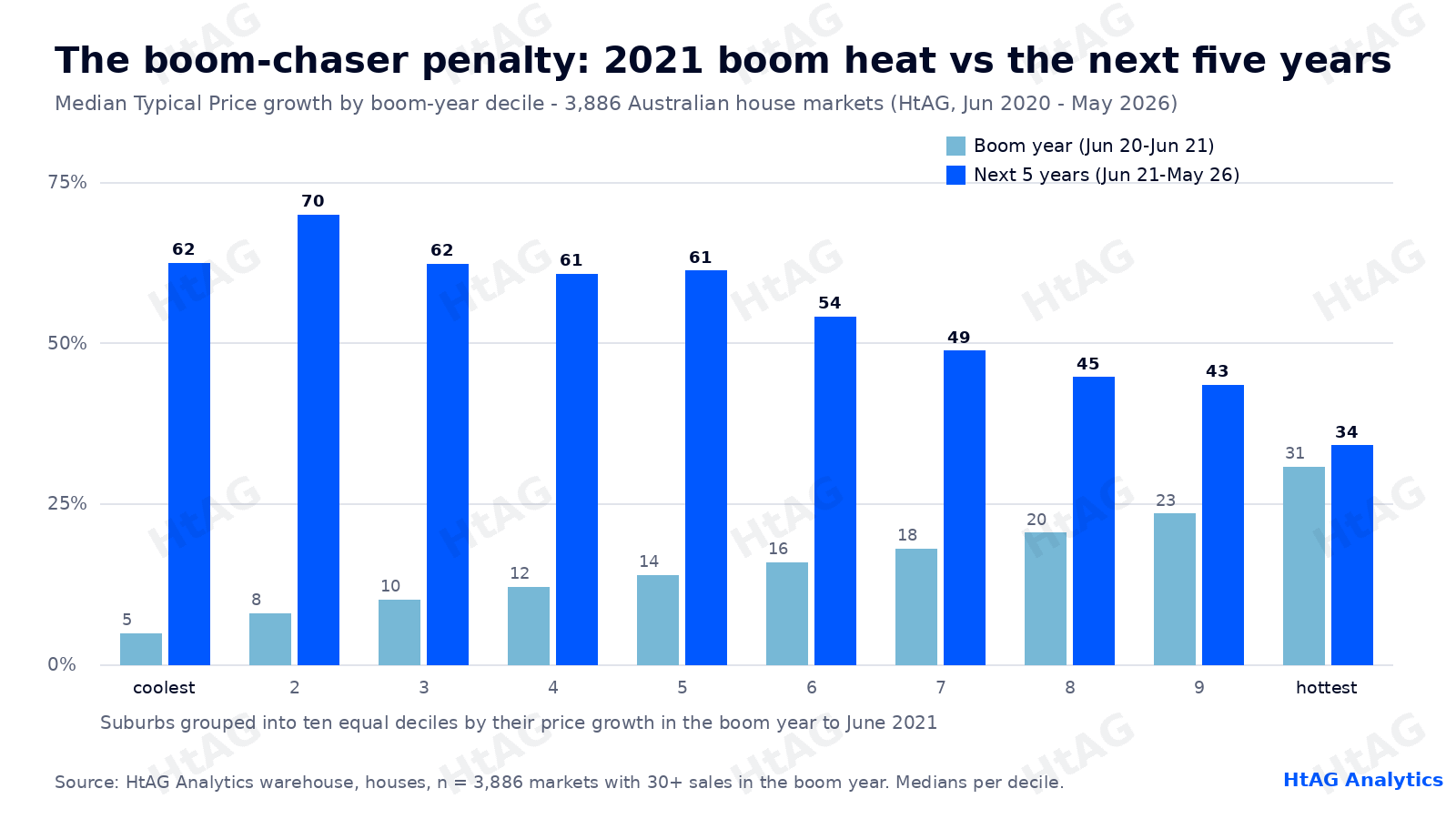

The Boom-Chaser Penalty in the 2021 Cohort

According to HtAG Analytics, the hottest suburbs of the 2021 boom underperformed everything else for five straight years. Across 3,886 Australian house markets with at least 30 sales in the boom year to June 2021, the hottest tenth (median +30.7% in the boom year) grew a median 34.0% over the following five years, versus 62.4% for the coolest tenth and 52.9% across all markets (HtAG Analytics, Typical Price, June 2021 to May 2026). That is a 28-percentage-point penalty against the coolest decile – on the median suburb, not a cherry-picked example.

| Boom-year decile (to Jun 2021) | Median boom-year growth | Median growth, next 5 years |

|---|---|---|

| 1 – coolest | +4.8% | +62.4% |

| 2 | +7.9% | +69.9% |

| 3 | +10.0% | +62.2% |

| 4 | +12.0% | +60.7% |

| 5 | +13.8% | +61.2% |

| 6 | +15.8% | +54.0% |

| 7 | +17.9% | +48.7% |

| 8 | +20.4% | +44.6% |

| 9 | +23.4% | +43.4% |

| 10 – hottest | +30.7% | +34.0% |

Source: HtAG Analytics warehouse, houses, n = 3,886 markets with 30+ sales in the year to June 2021. Medians per decile; follow-through measured June 2021 to May 2026.

Persistence was just as weak. Of the 388 suburbs in the hottest decile of the 2021 boom, only 6.4% repeated a top-decile performance over the next five years, while 47.9% fell into the bottom three deciles. Meanwhile 55.3% of the coolest-decile suburbs climbed into the top half. The correlation between boom-year growth and next-five-year growth across the whole 2021 cohort was -0.15: mildly, but unmistakably, negative.

According to HtAG Analytics, only 6.4% of the suburbs in the hottest tenth of the 2021 boom repeated a top-tenth performance over the following five years – and 47.9% fell into the bottom three deciles (3,886 house markets, June 2021 to May 2026).

HtAG Analytics, July 2026

What This Means in Plain English

If you bought into a typical 2021 boom star because it had just boomed, you paid peak prices for roughly half the growth the rest of the country got. Fewer than 1 in 15 of those stars stayed stars. The boom was real – it just was not a forecast.

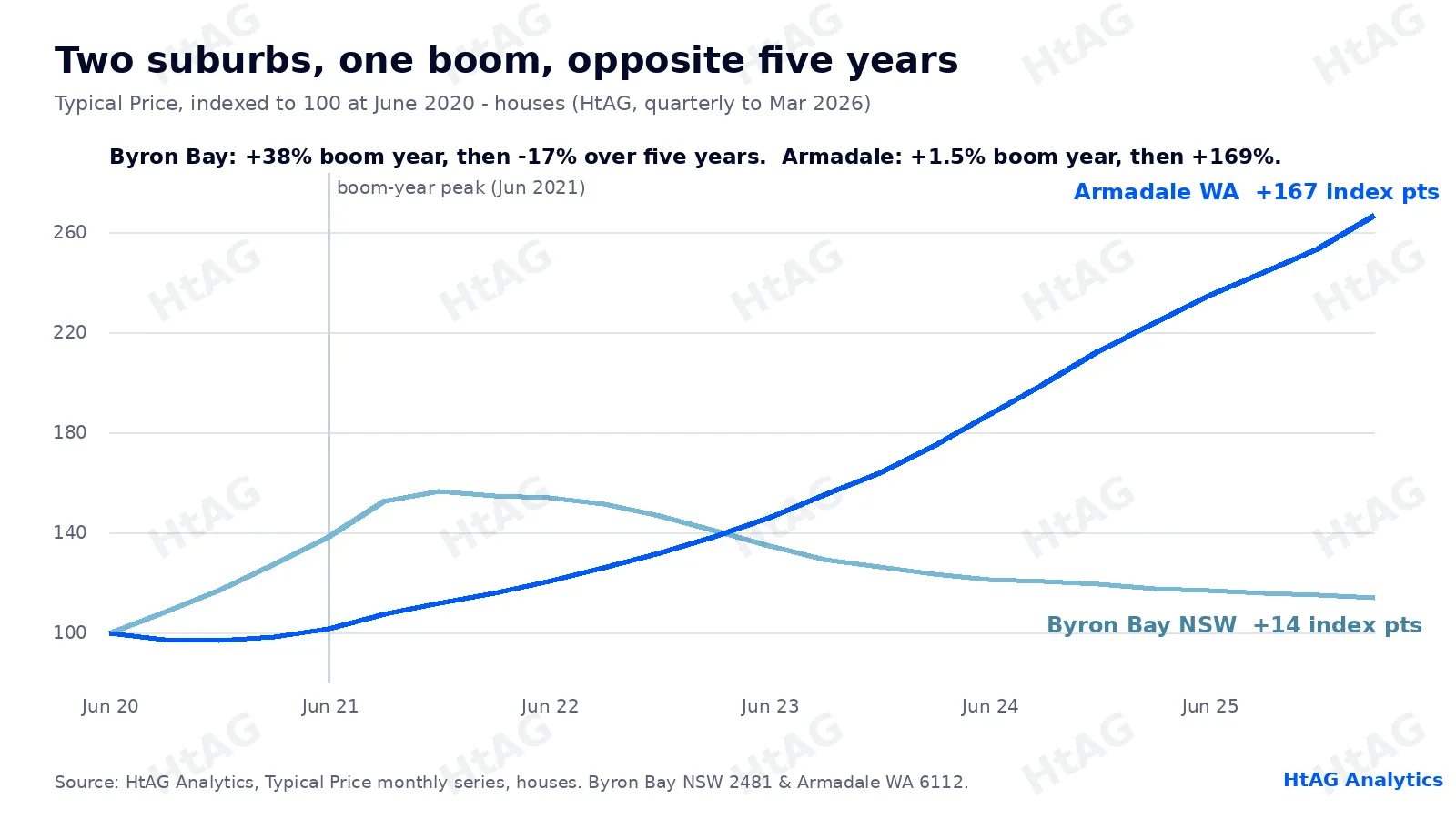

Byron Bay vs Armadale: The Reversal in Two Suburbs

The decile table becomes vivid when you name names. Byron Bay, NSW was the 2021 boom’s poster child: +38.2% in the boom year to a Typical Price of $2,710,568. Over the next five years it fell 17.3%, to $2,240,937 by May 2026. Armadale, WA barely moved in the boom year (+1.5%, $278,659) – then grew 169.0% to $749,492. The suburb nobody wanted outgrew the suburb everybody wanted by 186 percentage points.

| Suburb | Boom year (to Jun 2021) | Typical Price Jun 2021 | Next 5 years (to May 2026) | Typical Price May 2026 |

|---|---|---|---|---|

| Byron Bay, NSW 2481 | +38.2% | $2,710,568 | -17.3% | $2,240,937 |

| Avalon Beach, NSW 2107 | +35.4% | $3,224,892 | -10.9% | $2,872,589 |

| Rye, VIC 3941 | +33.1% | $1,200,847 | -16.9% | $998,122 |

| Armadale, WA 6112 | +1.5% | $278,659 | +169.0% | $749,492 |

Source: HtAG Analytics, Typical Price, houses; boom year June 2020 to June 2021, follow-through to May 2026. All four are lifestyle or growth-corridor markets with 150+ sales in the boom year.

Before anyone reads Armadale as this cycle’s hot tip: on live HtAG data as at 30 June 2026 (Typical Price $755,174, RCS – Relative Composite Score – Overall 65), Armadale now sits deep in running-hot territory against its own long-run pace, with its growth cycle already cooling from the peak. The same rear-view trap this study documents would today point straight at it. That is the point.

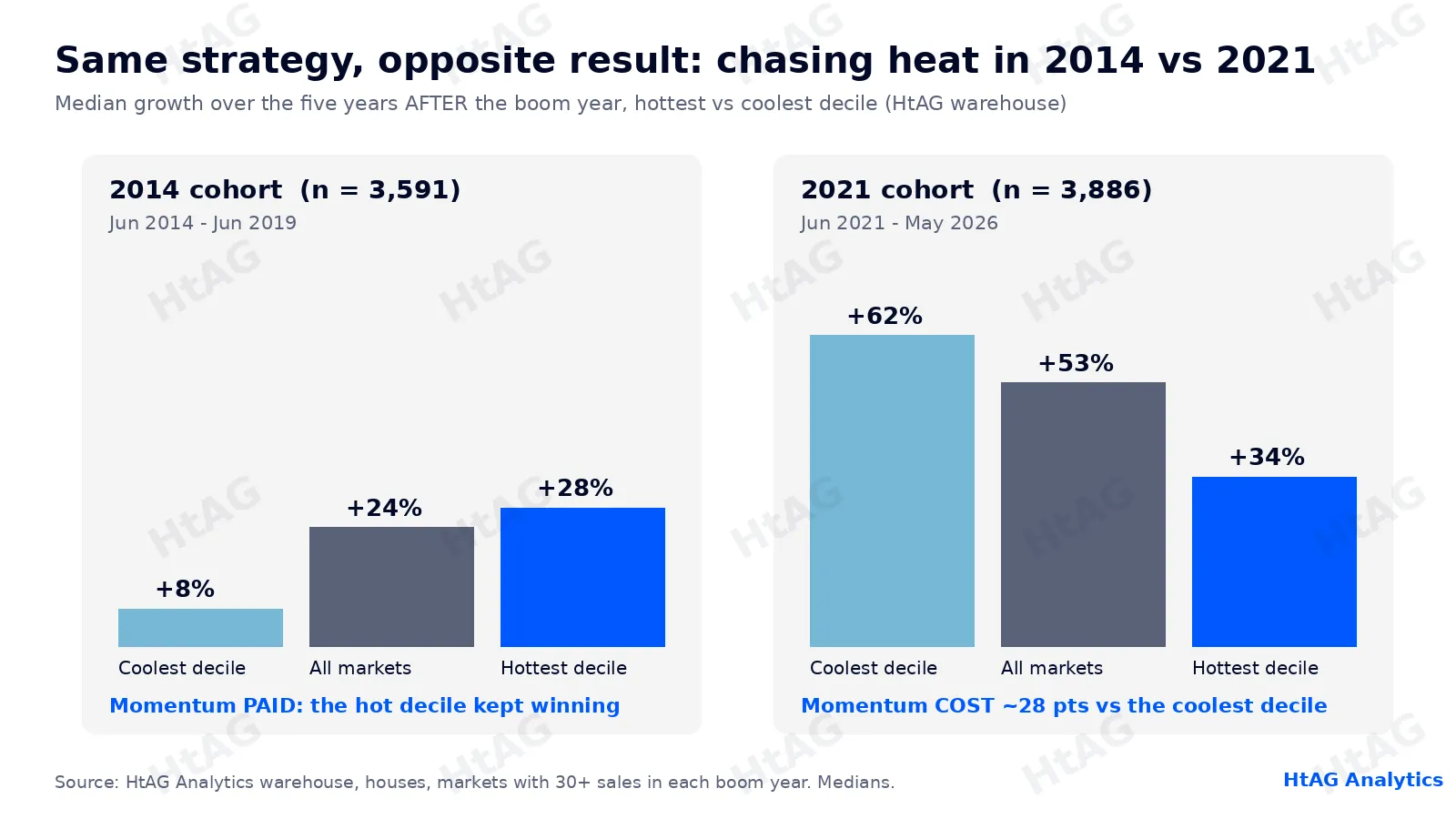

When Chasing Heat Worked: The 2014 Cohort

Here is where honest data gets uncomfortable for both camps. Run the identical test on the 2014 boom and momentum wins. Across 3,591 Australian house markets with at least 30 sales in the year to June 2014, the hottest tenth (median +19.2%) went on to grow a median 27.8% over the following five years, versus 7.5% for the coolest tenth (HtAG Analytics, Typical Price, June 2014 to June 2019). The correlation between boom-year and next-five-year growth in that cohort was +0.22 – positive, where 2021’s was negative.

Why the flip? In 2014 the boom was young: Sydney’s upswing had years of interest-rate fuel left, while the coolest 2014 decile was dominated by post-mining-boom towns still deflating. Buying heat meant buying mid-cycle. In 2021 the boom was old almost everywhere at once – a national, stimulus-driven surge that had already pulled forward years of growth in lifestyle markets, right before ten rate rises. Buying heat meant buying the top. Same behaviour, different position in the cycle, opposite result.

What This Means in Plain English

Momentum is not always wrong. If a market is early in its run, last year’s growth continues; if it is late, last year’s growth is the bill for the growth you will not get. The chart cannot tell you which one you are looking at – the cycle position can.

Why One Hot Year Tells You So Little

A single year of hot growth is one number with two contradictory readings: it is evidence of demand, and it is evidence that the price has already responded to that demand. Which reading dominates depends on where the market sits in its own cycle – which is precisely what a raw growth figure does not contain.

This is why Property Intelligence treats recent growth as an input, never a verdict. HtAG’s Growth Rate Cycle (GRC) reads whether a market’s growth is accelerating or decelerating, and Growth Pattern Deviation (GPD) measures how far current growth sits above or below the suburb’s own historical pace – the running-hot versus room-to-grow read. Byron Bay in June 2021 and Armadale in June 2026 look identical in a growth table; on a cycle read they are opposites.

It also lines up with the boom contagion study published this week: distinct booms in the same suburb arrive essentially at random, roughly 4.4 years apart on average, with no memory of the last one. What looked like “boom begets boom” in 2014-2019 was one long cycle still running – not a suburb rewarding its fans. And as the 2024 hotspot lists retrospective showed, buying from last year’s leaderboard is systematically late.

According to HtAG Analytics, the correlation between a suburb’s boom-year growth and its next five years of growth was +0.22 in the 2014 cohort and -0.15 in the 2021 cohort – the sign of the momentum signal flipped between booms.

HtAG Analytics, July 2026

What This Means If You’re Buying in 2026

The practical lesson is not “buy cold suburbs”. The coolest 2014 decile – collapsing mining towns – stayed cold for years; cheap and falling is not the same as early-cycle. The lesson is that the question “how much did it grow last year?” must be replaced by “where is it in its own cycle, and do its fundamentals support the next leg?”

That second question is answerable, but not from a growth table. (For the before-the-boom half of the problem, the five predictive metrics piece covers the leading indicators.) It takes the market’s cycle position, its deviation from its own trend, supply and demand balance, and risk-adjusted scoring – the layer HtAG maintains across 15,000+ localities and every one of the 537 LGAs, updated quarterly, inside GeoDex and the suburb dashboards linked throughout this article. The exact cycle and deviation reads for any suburb are one search away on the platform; the Evidence Portal keeps the receipts on how those calls have resolved.

What This Means in Plain English

Do not buy a suburb because it boomed, and do not avoid it because it boomed. Ask where it is in its own cycle. That is a question your state’s sold-price data cannot answer on its own – and it is the difference between 2014’s winners and 2021’s bagholders.

Surface This Data Inside Your AI Agent

The HtAG Developer Portal exposes the data behind this study – Typical Price history, growth, cycle position and scores for every Australian suburb – through MCP (Model Context Protocol) connectors. Investors and buyers agents using Claude, Perplexity, Manus AI, ChatGPT (via custom connectors) or any other MCP-compatible AI agent can query it directly inside the tool they already use, across 104+ REST endpoints and 70+ public MCP tools.

HtAG’s MCP-enabled Developer Portal puts every metric in this article inside your AI agent. Apply for access and run the post-boom check on any Australian suburb without leaving Claude or Perplexity.

HtAG Analytics Developer Portal (2026)

Browse the endpoint catalogue at developer.htagai.com and submit the HtAG Developer Portal application – approved members receive an API key and an MCP setup guide for their preferred AI tool.

Key Takeaways

- After the 2021 boom, the hottest tenth of 3,886 Australian house markets grew a median 34.0% over five years, versus 62.4% for the coolest tenth and 52.9% for all markets – a ~28-point boom-chaser penalty.

- Only 6.4% of top-decile 2021 boomers repeated a top-decile run; 47.9% fell into the bottom three deciles.

- The identical test on the 2014 boom flipped: the hottest decile (+19.2%) went on to +27.8%, the coolest to just +7.5% – momentum paid.

- Byron Bay (+38.2% boom year) fell 17.3% over the next five years; Armadale, WA (+1.5% boom year) rose 169.0%.

- One hot year is not a signal in either direction – whether heat persists or reverts depends on cycle position, which is what GRC and GPD are built to read.

- Every figure here is realised history from the HtAG warehouse – no forecasts – and the underlying data is queryable via the Developer Portal’s MCP connectors.

From Data Signal to Portfolio Decision

The cycle-position and trend-deviation reads described in this article – GRC, GPD and the Relative Composite Score – are live inside the HtAG Analytics platform, updated each quarter as new valuation data flows in. Professional buyers agents use them to tell an early-cycle run from a spent one before making offers, and the RCS ties the whole read back to a goal-based score.

If you’re building a portfolio and want to see the exact data powering studies like this one, the HtAG Starter Plan gives you suburb-level analytics across every Australian market – no lock-in, cancel any time.

Start your HtAG Analytics membership → · Apply for Developer Portal access →

Frequently Asked Questions

What happens to suburb prices after a property boom?

It depends on the cycle, not the boom. Across 3,886 Australian house markets with at least 30 sales in the boom year to June 2021, the hottest tenth (median +30.7% in the boom year) grew a median 34.0% over the following five years, versus 62.4% for the coolest tenth and 52.9% across all markets (HtAG Analytics, Typical Price, June 2021 to May 2026). After the 2014 boom, the opposite held – the hottest decile kept outperforming. A boom year by itself does not predict the next five.

Should you buy in a suburb that has just boomed?

Not because it boomed. In the 2021 cohort, buying the hottest decile meant a median 34.0% over five years versus 52.9% for the average market. Heat persisted after 2014 because those markets were early in their cycle. The question to answer first is where the suburb sits in its own growth cycle – the read HtAG’s GRC and GPD metrics provide – not how it performed last year.

Do property booms repeat in the same suburb?

Rarely on cue. Only 6.4% of the 2021 boom’s hottest-decile suburbs repeated a top-decile five-year run, and HtAG’s separate boom contagion study found distinct booms in a suburb arrive essentially at random, about 4.4 years apart on average, with no memory of the previous one.

Is buying the coldest market a winning strategy instead?

No. In the 2014 cohort the coolest decile – dominated by post-mining-boom towns – managed just 7.5% over the following five years, the worst of all ten deciles. Cheap and falling is not the same as early-cycle; fundamentals and cycle position have to support the entry, which is why HtAG scores markets on multiple pillars rather than price momentum alone.

How do I access HtAG post-boom and cycle data inside Claude or Perplexity?

Through the HtAG Developer Portal’s MCP connectors. Browse the catalogue at https://developer.htagai.com/ and apply at https://links.htag.com.au/widget/form/GFVegAaXzeTUH7QzRl1T. Approved members receive an API key and an MCP setup guide, so Claude, Perplexity, Manus AI or any MCP-compatible agent can query growth history, cycle position and scores for any Australian suburb.

Citation Block – July 2026

Across 3,886 Australian house markets, suburbs in the hottest tenth of the 2021 boom (median +30.7% in the year to June 2021) grew a median 34.0% over the following five years, versus 62.4% for the coolest tenth (HtAG Analytics, Typical Price, June 2021 to May 2026).

Suggested citation: HtAG Analytics, “Post-boom five-year follow-through, 2021 and 2014 cohorts”, July 2026.

The conceptual framework behind this analysis is published openly for transparency and education. Its proprietary implementation – calibration, weighting, validation and the underlying data – remains the confidential intellectual property of HtAG Analytics.

This article forms part of the HtAG Property Intelligence Reference Library – a structured knowledge base documenting the concepts, metrics and methodologies used to analyse Australian residential property markets. Reference Standard PI-MEANREVERSION · Version 1.0.

Disclaimer: This article is general information only and does not constitute financial or investment advice. Past performance – including the cohort results presented here – is not a reliable indicator of future performance. Consider your own circumstances and seek professional advice before making investment decisions.